The bottoming process continues.

BTC sits at ~$62K after a month defined by equity market volatility, hawkish Fed posturing, record BTC ETF outflows, and heavy uncertainty surrounding Michael Saylor's Strategy. It was a stress test on multiple fronts, and while price took the hit, ending the month down roughly 12%, the resolution of the Strategy overhang and a rapidly improving inflation picture leave us more constructive exiting June than we were entering it.

Below, we review the macro shift underway, the Strategy saga and its resolution, the most significant TradFi stablecoin development to date, and why Solana's resurgence continues to validate RockawayX’s core thesis.

Macro Backdrop: The Data vs. The Fed

The inflation data is telling investors the worst is behind us, in stark contrast the Fed Chair Warsh’s biases.

Truflation, the real-time inflation measure we've referenced in past notes, peaked in late May and has been rolling over since. The 5-year breakeven rate, the difference between the on-the-run 5yr rate and the 5y TIPs coupon, a popular measure of future inflation, has fallen more than 50bps over the past eight weeks, back to lows not seen since last December. And the driver of the entire inflation scare brent oil out of the Strait of Hormuz, has reversed decisively: Brent crude has fallen to just $70 per barrel, down from a high of $113, as the Strait of Hormuz has reopened and markets see a path to a permanent ceasefire between the US and Iran.

Despite significant evidence of disinflation, Fed Chair Warsh was sharply hawkish in his first FOMC meeting, which subsequently flipped market expectations to a hike from cuts. Markets came into 2026 expecting 2.5 rate cuts, but left Warsh’s pressure expecting a full rate hike. Moreover, the Fed governors are split on the forward path of rates, at the same time that Warsh is expected to eliminate or significantly pair back forward guidance.

On balance, we believe the forward rate path is uncertain and mixed. With hikes now priced and the hard data rolling over, the burden of proof has arguably shifted to the hawkish case. Whether Warsh's framework proves prescient or premature, the coming months of inflation prints & high frequency data will settle the question more decisively.

The Strategy Saga: From Overhang to Resolution

Crypto majors and select alts held up remarkably well in June given the environment of record BTC ETF net outflows, volatile equity markets, a hawkish debut from Fed Chair Warsh, and, most consequentially, a crisis of confidence in the market's largest price-insensitive buyer, Michael Saylor.

Michael Saylor’s Strategy started the June month by selling a small amount of BTC to fund STRC dividends. This surprise added to the uncertainty posed by Strategy in May when it repurchased $1.5B of its 2029 convertible note, meaningfully impairing cash runway to around 6 months. The move cast heavy uncertainty into crypto markets: STRC depegged from its $100 target and MSTR ultimately fell below 1x mNAV. The market's concerns were threefold: a) it cast doubt on Saylor as an indefinite price-insensitive buyer of bitcoin, b) it implied he may be willing to sell large amounts of BTC to fund higher STRC dividends or the convertible bonds due next year, and c) with mNAV below 1.0, Strategy could no longer tap its ATM facility to fund future purchases. The reflexive machine BTC purchases that supported the prior bull market appeared to be in jeopardy.

On June 29th, Saylor moved to calm markets. Strategy's board approved a "Digital Credit Capital Framework" with five components:

- a formal US dollar reserve policy,

- a revised STRC dividend policy,

- a $1B buyback program for its preferred securities,

- a $1B buyback program for MSTR common stock,

- and a bitcoin monetization program.

The STRC dividend was subsequently raised from 11.5% to 12%, and the company set its dollar reserve at ~$2.55B, roughly 17.4 months of coverage against ~$1.76B in annual preferred dividend and interest obligations. The board authorized up to $1.25B of BTC sales to rebuild that reserve, bringing total interest coverage to ~$3.8B, or nearly 26 months. Critically, the company adopted a policy requiring a minimum dollar reserve of 12 months of obligations, any breach of which requires board authorization, and stressed that the program does not require it to sell any bitcoin.

The framework gave certainty to the market - Saylor will sell some BTC when necessary. But we read the announcement as constructive, and the market agreed: off their lows, both MSTR and STRC rallied 23% on the news as of the July 2rd market close. Strategy now sits at an mNAV of 1.08, up from 0.99. The framework replaced an open-ended uncertainty with a defined, capped, and rules-based program. BTC fell to a low of $57.7K amid the turmoil but rallied back to ~$62K on the back of the announcement, ending the month down ~12%, but ending the week positive as the market finally had clarity on Strategy financing plan.

We reiterate the view from our May note: Strategy is not a forced seller. Total debt plus preferred and convertible debt remain a small fraction of its 847,000+ BTC holdings. With the capital structure question largely answered, we believe Strategy will return as a net buyer.

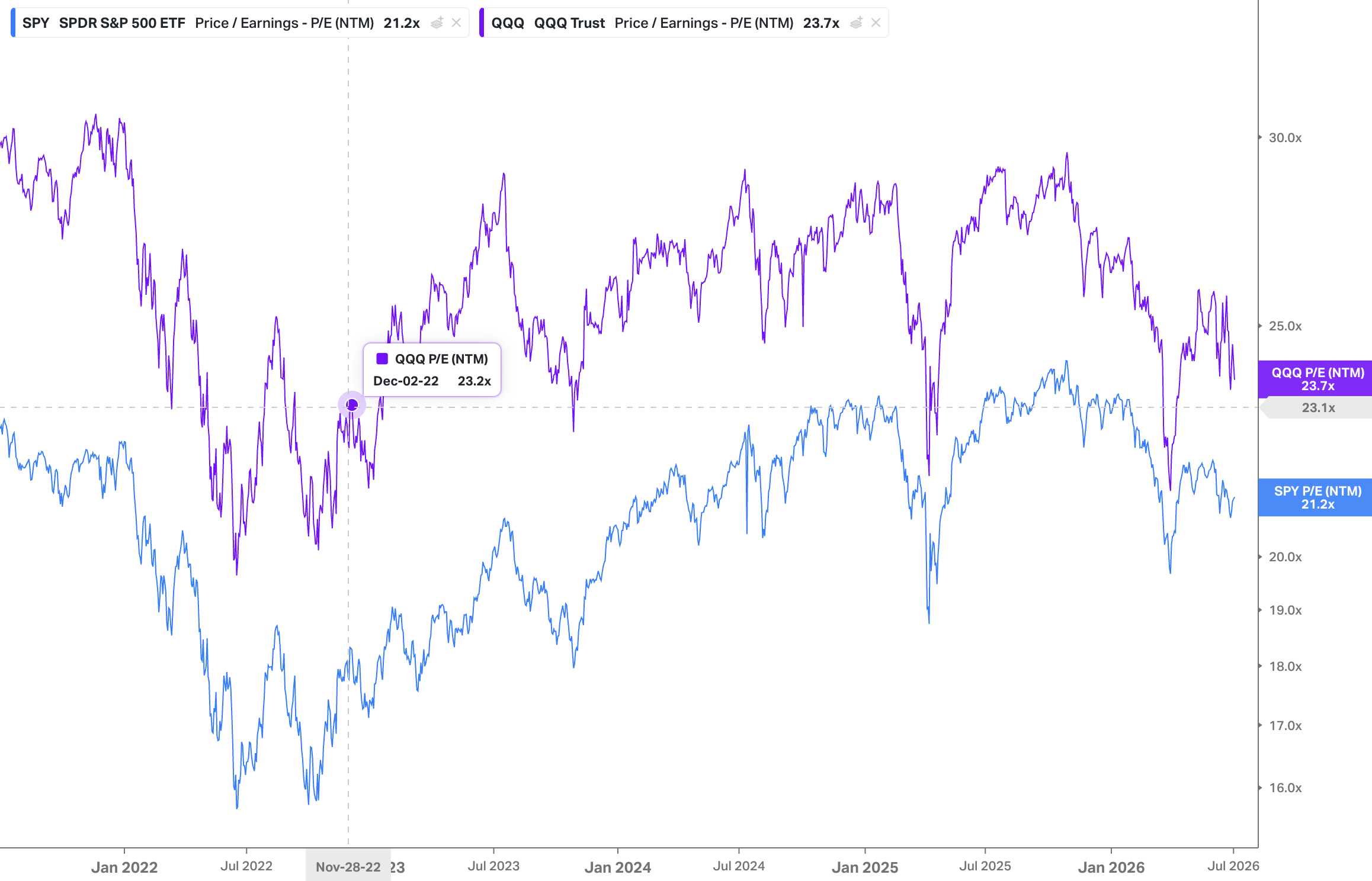

US Equity Market "Bubble" Fears Are Misplaced

With crypto still positively correlated to equities, a US stock market bubble would be a genuine risk to crypto prices. We believe these bubble fears are misplaced.

Historically, bubbles are characterized by expanding valuation multiples - the realization of price getting ahead of fundamentals. However, both the Nasdaq and S&P 500 have seen their valuations contract since the start of the year. Moreover, and remarkably, the Nasdaq’s valuation is essentially flat over the entire period since ChatGPT launched in November 2022. Prices have risen, but earnings have risen faster. At the index level, last quarter's financial results were exceptional. As we mentioned in a previous note, the S&P 500 realized index-level aggregate YoY earnings growth of 28%, strength that is unheard of in a mid-cycle environment.

Bubbles are defined by multiple expansion detached from fundamentals, and this market is exhibiting the opposite.

OpenUSD: The Most Significant TradFi Crypto Adoption Development to Date

On June 30th, a consortium of tradfi juggernauts announced OpenUSD (OUSD), a new US dollar-pegged stablecoin backed by 140+ partners including Visa, Mastercard, Stripe, BlackRock, Coinbase, Google, Shopify, BNY, and Standard Chartered, with Stripe planning to make OUSD the default stablecoin for its merchant network.

We do not use the word "significant" lightly. OpenUSD's design is in sharp contrast to the single-issuer model that has dominated crypto and has left investors scratching their heads over how stablecoin market fragmentation will evolve.

Rather than one issuer controlling the economics of OUSD (e.g. Circle with USDC, Tether with USDT), OUSD is designed as shared infrastructure across banks, fintechs, payments firms, and crypto-native players. The deal for users is attractive as there are mint/redemption fees. Most importantly, the majority of treasury reserve yield will be shared amongst consortium partners after a management fee. The market immediately understood the competitive implications: Circle's stock fell over -15% on the news.

Stepping back - we cannot understate the significance of this annoucement. The largest payments, banking, and asset management firms are embracing crypto rails with open arms and stand to economically benefit from a collectively embracing crypto rails.

The backdrop makes the growth even more impressive: the GENIUS Act is not yet fully implemented and degrees of regulatory uncertainty persist, with rulemaking expected to commence in Q3 2026 to Q1 2027. We think tradfi banks and fintechs can’t wait to get stablecoins into their users hands. Once GENIUS rulemaking is finalized, we expect stablecoin supply to inflect meaningfully higher.

Solana Resurgence

Solana TPS shot up to weekly all-time highs in June on the back of several several different market verticals - spot equity RWAs, collectibles, and memecoins.

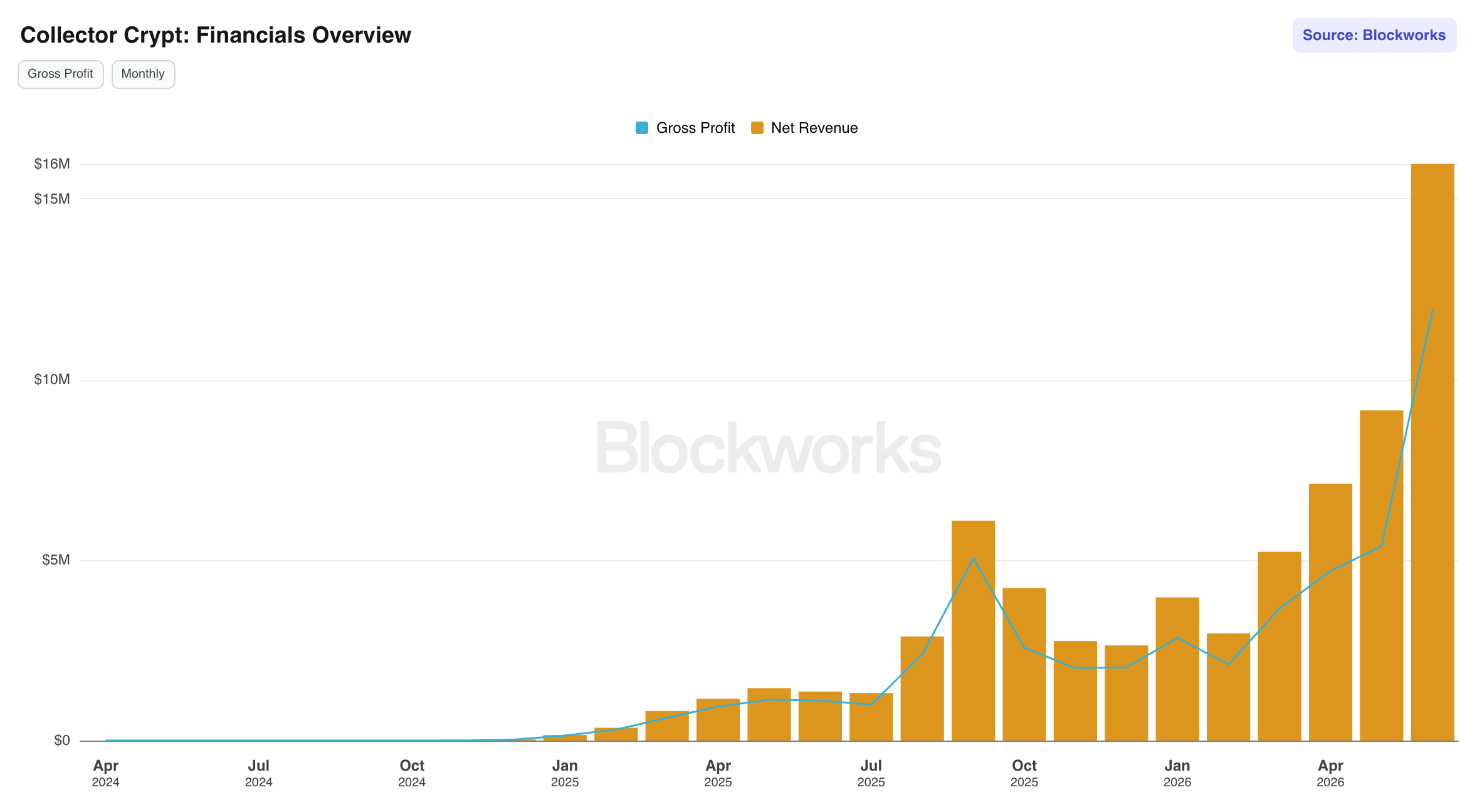

SPCX, MU, SDNK and DRAM drove tokenized equity trading on Solana to a new ATH of $3.6B, a month-over-month increase over over 220%. The memecoin trenches saw a genuine resurgence, driven by the new Ansem token. And trading & gacha spend on Collector Crypt, the popular collectibles platform we flagged in our April note, reached all-time highs.

We believe this recent ‘Solana Resurgence’ is just another validation of our Solana thesis. The strength, diversification, and quality of Solana's developer & user base is unmatched. Solana remains the only chain in crypto that houses this many high-velocity, high-revenue use cases simultaneously - collectibles, tokenized equities, memecoins, DeFi - each with distinct user bases and demand drivers. We fully expect Solana to maintain its dominance into the next bull market, with new ATHs across KPIs, as it again proves itself the best chain for retail traders and best-in-class founders.

SPCX & Memory Stocks: Driving RWA Volumes

Solana and Hyperliquid were the primary beneficiaries of recent IPO activity and stock market volatility in June. The SPCX listing and the popular AI memory trades (MU, SDNK, DRAM) pushed Solana Sunrise - an issue of spot equity assets on Solana - spot equity volumes and Hyperliquid RWA perps open interest to new all-time highs. The onchain data continues to validate our RWA thesis: the market for RWAs is TAM-expansionary for crypto.

Downside Risks: A Critical Period for CLARITY

The CLARITY Act is stuck in the Senate, with prediction markets pricing a ~40% chance of passage by year end. Due to the mid-term elections this year, July is a make-or-break month for the bill, which could introduce near-term volatility.

One of the bill's most contentious provisions is designed to protect non-custodial software developers from being treated as money transmitters merely for writing open source defi code. Several US law enforcement groups are arguing it could create AML and enforcement gaps that bad actors could exploit. The emerging compromise appears to be narrow revisions that preserve core protections for legitimate developers while making clear that actors who knowingly facilitate illicit activity remain subject to liability. It’s tbd on how this provision shakes out. The second major issue is around an ethics provision aimed at President Trump’s crypto ventures. The Trump family’s recent disclosure of over $1.4B in crypto-related income will not making passing CLARITY any easier. Lastly, while the question of stablecoin yield paid to holders is believed to be resolved, it coming back into focus cannot be ruled out.

The crypto industry has just four critical weeks, July 13th through Aug 7th, to get the bill through the Senate. The bill passed the House in 2025 and cleared the Senate Banking Committee, and was placed on the Senate Legislative Calendar on June 1st. But it still needs floor time for debate and amendments, a path to 60 votes to overcome a potential filibuster, and continued negotiation among stakeholders including the White House and industry groups.

Senate floor time is scarce and fiercely competed for. Once lawmakers leave for the August recess, attention will shift toward the November midterms elections, and passing significant bipartisan legislation becomes much harder, or impossible at worst. A failure to pass CLARITY this summer wouldn't kill the secular bull case for crypto, but it could push the industry's most important legislative catalyst well into next year. We think this prospect could present downside risk. Moreover, it’s not clear to us whether or not CLARITY will pass this year or next. We see strong arguments and evidence both ways.

Closing Thoughts

June delivered another stress test, and while BTC and alts suffered volatility, we believe they emerged on the other end much stronger. The largest corporate holder of bitcoin publicly confronted its capital structure and emerged with a credible, rules-based framework for balance sheet management. Inflation expectations are collapsing even as the Fed talks tough, setting up a policy pivot that should support risk assets. The world's largest payments and banking institutions just committed to stablecoin rails at unprecedented scale. And Solana's activity is hitting all-time highs across multiple independent verticals in the middle of a bear market.