Volatility = Opportunity

Over the past two months, we were impressed with the observed strength of crypto in the face of unprecedented defi hacks and heightened geopolitical conflict. BTC, ETH and HYPE had outperformed equities since the start of the UR-Iran conflict, but have given back that outperformance and then some, with the exception of HYPE which remains outperforming on a relative basis.

The Nasdaq 100 is -5.5% off its highs, and total crypto market cap is down just over -50% from its high reach this past October. We believed we were at a bottom in the crypto market, but BTC now sits just below its February 2026 low at roughly $61k. These are levels that we have not seen since before the US election in October 2024.

Below, we review the recent volatility, some go-forward risks, and, ultimately, why these markets are ripe for opportunity.

Volatility

We see two factors as the reason for the recent selloff in BTC, which has sparked a continued sell-off in crypto assets broadly: an absence of the DAT bid & perceived quantum risk.

The DAT bid

For much of the last leg higher in BTC, the DAT complex was the dominant and largely price-insensitive buyer. The market feared the Saylor bid was gone because Strategy sold 32 BTC to fund the STRC dividend on June 1. Saylor resumed purchasing BTC this week - over $100M in size - yet this was enough to scare market into derisking.

Quantum

The quantum narrative is also getting more airtime, adding to the overhang, even if the real timeline remains far into the future. The market perceives bitcoin core devs as behind the curve with respect to quantum preparedness. Organizations like Google, Cloudflare, and the Ethereum Foundation have set 2029 as a public target for migration to post-quantum cryptography. Bitcoin, by contrast, remains stuck in draft stage with no activated timeline or unified roadmap, and little communication to the market to ease investor fears. Many fear that governance and philosophical gridlock could leave its migration lagging behind quantum timelines.

How Risks Reverse

While these perceived risks may induce volatility over time, we’re looking for upside risk as these fears subside.

We stress that Strategy is by no means a forced seller of large amounts of BTC - Strategy’s total debt plus preferred shares are just ~35% of total BTC owned, the STRC dividend can be deferred indefinitely, and Saylor retains the ability to raise capital via ATM sales. As such, we believe that fear around outsized sales from Strategy are overblown. Importantly, with think crypto prices can whipswap higher if Strategy returns to the market as a buyer of bitcoin in size.

We also believe quantum fears may subside quickly and unexpectedly. There are is a lot market cap at stake with bitcoin, so the industry at large is highly incentivized to solve the problem. Worse case, industry leaders like Coinbase, Binance, and Blackrock can force change at the social layer by pressuring the crypto community to act and mitigate quantum risk.

Strong Macro Backdrop

In contrast to crypto, the tradfi & macro backdrop remains very constructive, with strong GDP growth, exceptionally strong earnings momentum, and tame inflation. Equity markets have been very constructive, and the Nasdaq is in the midst of a statistically expected pullback, which we view as healthy and necessary correction.

The US remains in an AI-driven cyclical upswing, where AI demand is not only resulting in companies like Anthropic posting some of the most impressive result in financial history, but also driving record data center spend, accounting for most of the growth in the US. The ISM PMI, a trusted measure of manufacturing growth, posted its 5th straight month of expansion, its best streak since 2022, after nearly two years of contraction.

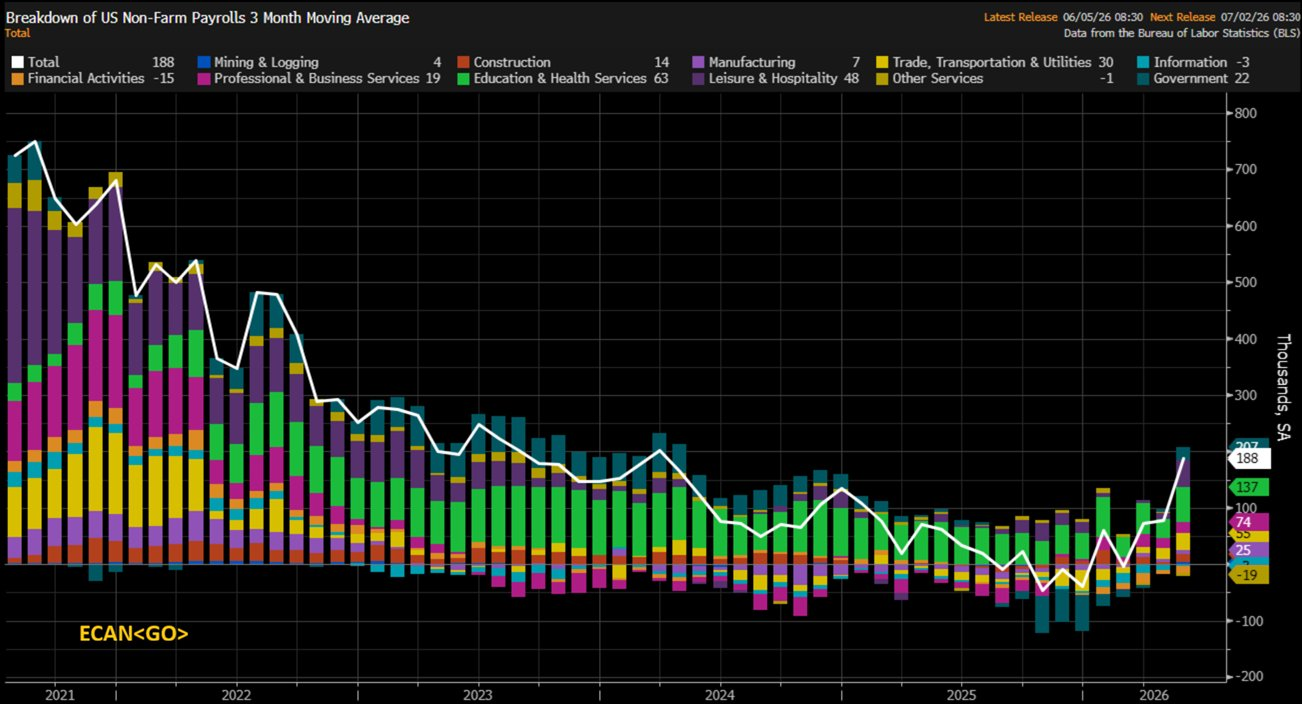

As a consequence, the job outlook remains highly constructive. The May US jobs report blew away expectations, with the US economy gaining 170k jobs versus a consensus estimate of just 80k, and the U3 unemployment rate holding steady at 4.3%. As we’ve mentioned in past notes, the data continues to invalidate fears of AI-induced unemployment. Recent US Non-farm Payroll gains have been so strong they’ve broken the 5-year downtrend in the measure.

Inflation is a risk we are monitoring (more on this below), but it remains subdued despite higher oil prices. Here we look to Trulfation, , non-BLS inflation index that measures price changes in near real-time millions of price points pulled daily from sources like retail listings, commodity prices, and other transactional feeds.

Truflation began to run high in response to the US-Iran conflict, but the measure has cooled recently as oil prices have stabled in the 90-100 USD range. It’s far too early to tell, but given the incentive of the Trump Administration to close a deal with Iran before US mid-term, we’re hopeful the worst of the US-Iran inflation scare is behind us.

Looking Ahead

When price action and fundamental data are strong, it’s important to look forward to potential risks.

Geopolitics & Oil

The confluence of geopolitical risk, higher oil prices, and a new Fed chair may spell volatility for tradfi risk assets and therefore crypto from a correlation perspective.

The US-Iran War, if prolonged, could impede business confidence & investment. Net energy exporters like the US may actually gain on net from higher oil prices (and falling natgas prices). But Regions like the EU and APAC could start to see an economic slowdown if prices stay higher for longer. If their slowdowns are acute enough, the weakness could spread globally, though we have our doubts about this given the US’ relative strength and size on the global stage.

The Fed & Rates

We also see the potential for the market to begin testing new Fed Chair Kevin Warsh, and we may be in the early innings of that today.

Warsh has stated his intentions to employ less forward guidance and modernize how the US measures inflation. Some of these changes may be welcome, but others could create risk. Markets prefer certainty, so less forward guidance could push risk premiums higher and leave markets more volatile than they otherwise would be. Rates are already pricing in a “higher for longer” environment due to strong US growth an elevated energy prices. A lack of forward guidance could add fuel to the fire.

New IPO Supply Shock

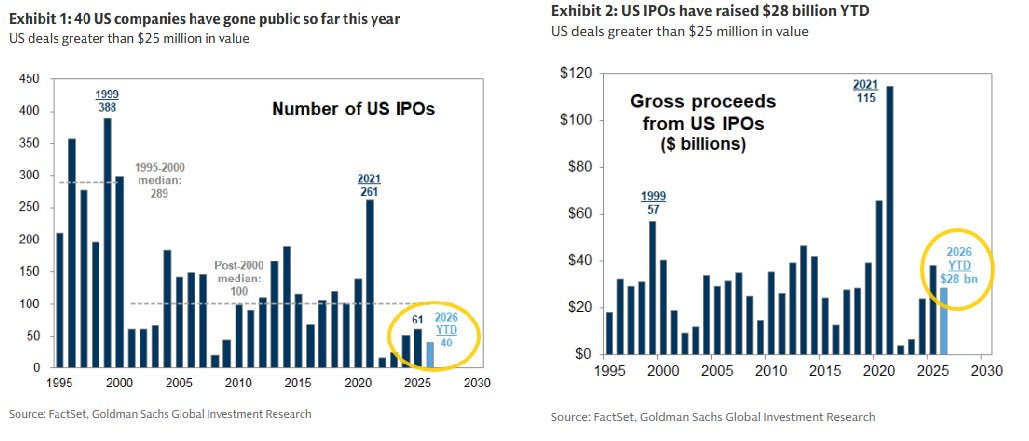

The IPO market is poised for a significant acceleration in 2026, with Goldman Sachs forecasting $225 billion in gross proceeds, roughly six times the $38 billion raised in 2025. The wave of upcoming megacap listings will introduce substantial new equity to the market. We believe the picture is far less daunting when viewed in historical context.

As a percentage of total market cap, 2026 issuance is expected to equal just 1% of Russell 3000 market cap, in line with 2015 to 2019 levels and low by historical standards. In dollar terms, projected proceeds remain well below the 1999 and 2021 peaks, and YTD activity has been muted with only 40 US IPOs and $28 billion raised through this point in the year.

Importantly, US capital markets are exceptionally deep, and we believe they are well positioned to absorb new supply, especially for such high quality companies. Total US fixed income outstanding now exceeds $50 trillion, and alternative assets have grown into a $20 trillion-plus asset class. Nearly half of total equity market cap is managed by passive instruments that purchase equities regardless of the market environment, providing a structural, price-insensitive bid. The confluence of this market depth and a large passive investor base makes us considerably less concerned about new equity supply.

Opportunity

We believe select crypto assets are very mispriced. We think the majors - BTC, SOL and HYPE, are undervalued relative to their long-term adoption trajectories and the structural demand building beneath them.

This dislocation is precisely the kind of opportunity we are positioned to capitalize on.

Bitcoin

BTC now sits at prices not seen since before the US election in October 2024, yet the bull case for bitcoin has never been stronger. The regulatory backdrop has shifted decisively in bitcoin's favor, and the world's largest asset managers are now formally underwriting it as a portfolio asset.

Global asset managers are integrating bitcoin into the model portfolio allocation. Blackrock has published guidance recommending a 1-2% allocation to BTC in traditional multi-asset portfolios, arguing its risk contribution at that size is comparable to holding a megacap tech stock. When the largest allocators in the world are integrating bitcoin into traditional asset allocations, we can say BTC’s value proposition as a non-sovereign store of value is no longer fringe. This institutional tailwind, paired with a constructive regulatory environment, is a structural tailwind that simply did not exist in prior drawdowns.

What’s more, we’re viewing the 4-year cycle is a possible catalyst for the timing of the recovery. BTC is tracking its familiar trajectory of massive gains followed by a 12-24 month bear market, and if that pattern repeats, the allocation decisions investors make today will determine the money made in the incoming bull market.

Solana

Solana is now exhibiting a meaningful advantage in onchain execution efficiency in certain trade sizes and pairs versus centralized exchanges and is solidifying itself as the home of onchain spot equity trading.

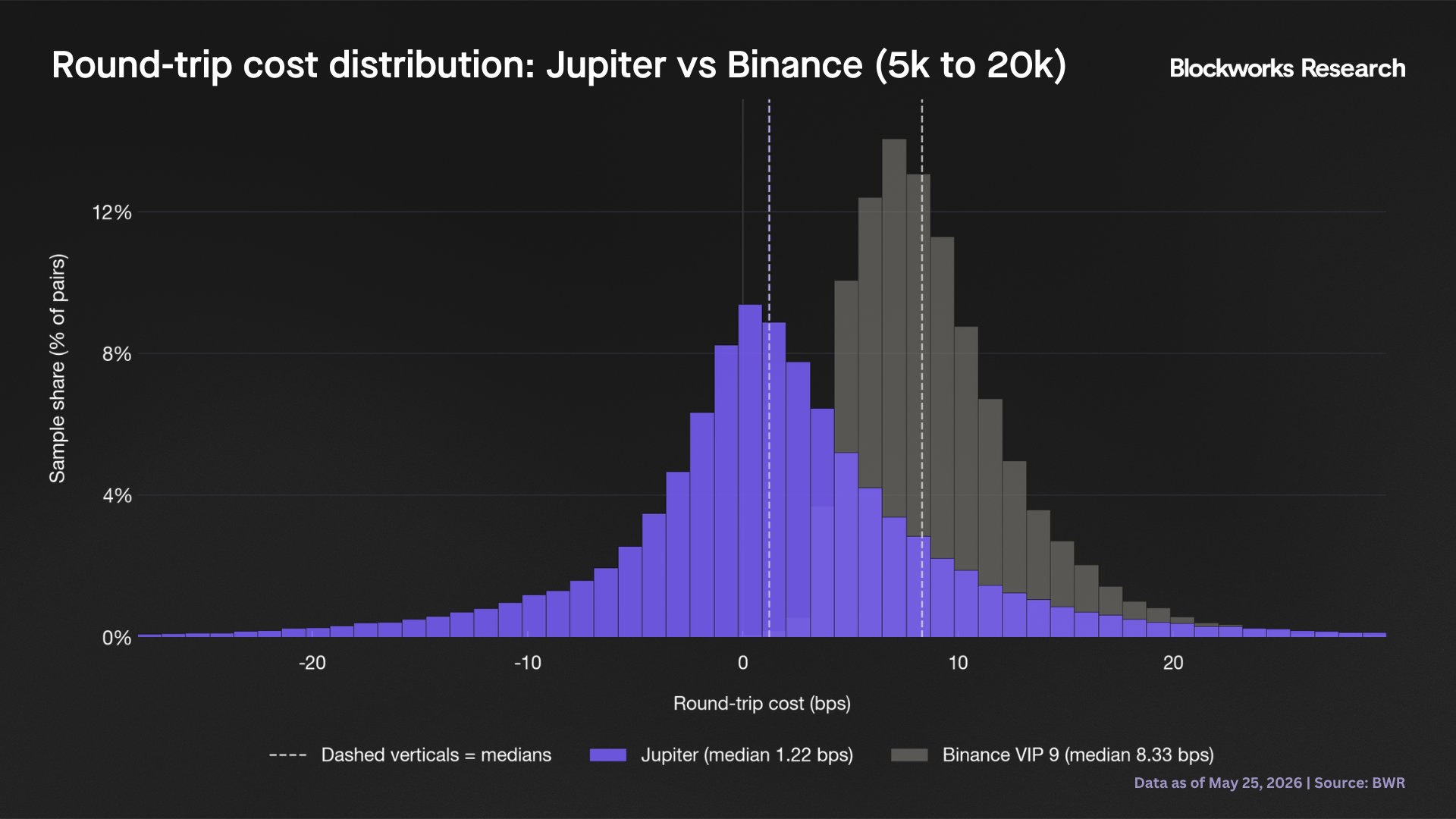

Per Blockworks Research, median SOL-USDC fills routed through Jupiter, the top trading aggregator on Solana, have consistently landed inside Binance's top VIP tier since late last year, frequently beating the raw CEX reference price before fees are even applied. We’re seeing early evidence that this dynamic is beginning to extend to BTC and longer-tail assets. On the equities side, the recent Securitize-Jump-Jupiter partnership to launch regulated tokenized equity trading on Solana, alongside the CLARITY Act's advancement out of the Senate Banking Committee, positions the network to capture spot equity flow as the asset class migrates onchain, adding to Solana’s lead in spot equity trading versus competing blockchain.

On a forward basis, technical upgrades on Solana over the next 12 months should make it even more competitive on execution costs versus centralized exchanges. We think key technical updates like BAM and lower slot times could make Solana competitive for perpetual futures trading, an area where it has historically lagged. If Solana can pull this off, it could lead to significant fee revenue and a re-rating of the SOL token. The market is mispricing this future state.

Hyperliquid

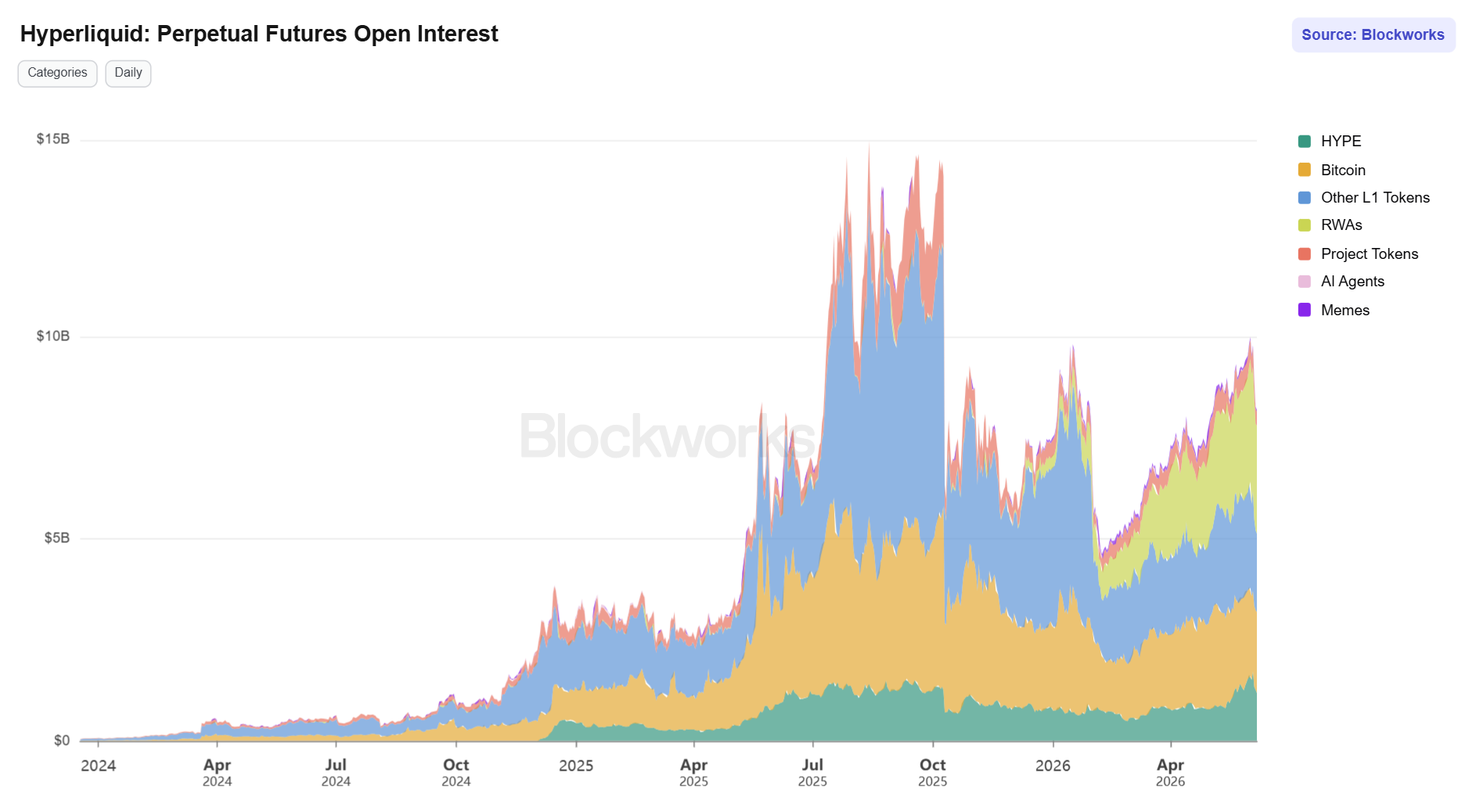

Hyperliquid continues to generate mainstream attention, open interest on the platform is recovery nicely since the 10/10 selloff, driven by a surge in RWA OI. Hyperliquid appears to be solidifying itself as the onchain venue for crypto natives to trade stocks and commodities with high leverage.

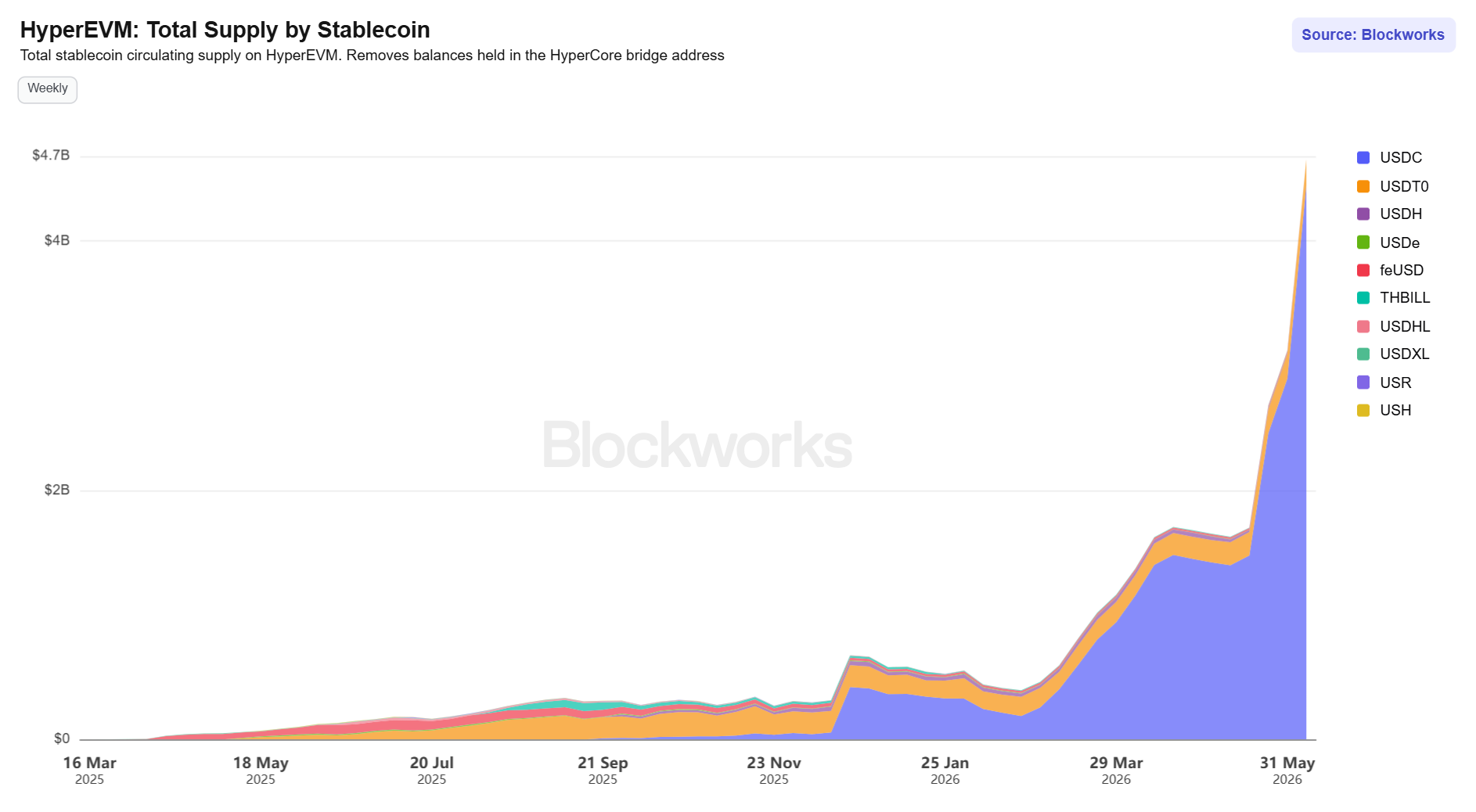

Most importantly, we’re witnessing its HyperEVM ecosystem attract an increasing amount of builder talent and users are bridging stablecoins into the ecosystem, which we believe are leading indicators of HYPE price performance.

Looking Forward

The crypto market has handed back its hard-won outperformance, but the forces behind the selloff - a paused DAT bid, quantum narrative, and equity market strength - are far more reversible than the price action suggests. Strategy is no forced seller, the industry is deeply incentivized to neutralize quantum risk, and the broader macro backdrop remains as constructive as we've seen in years.

Against that setup, BTC trading at pre-election 2024 levels, SOL valued as though its adoption never happened, and Hyperliquid quietly compounding builder momentum strike us as obvious dislocations - a commonality of crypto bear markets. History suggests the allocation decisions made in moments like this define the returns of the cycle that follows. We remain optimistic but vigilant. And, above all, positioned to act.