Centrifuge is a blockchain for tokenization of real-world fixed-income assets, such as invoices, royalties, and mortgages. The blockchain is built on Polkadot and connects to Ethereum via a bridge. The first application on the Centrifuge network, Tinlake, brings real-world yield to the DeFi ecosystem by letting customers borrow against their tokenized real-world assets.

BUSINESS MODEL

Tinlake

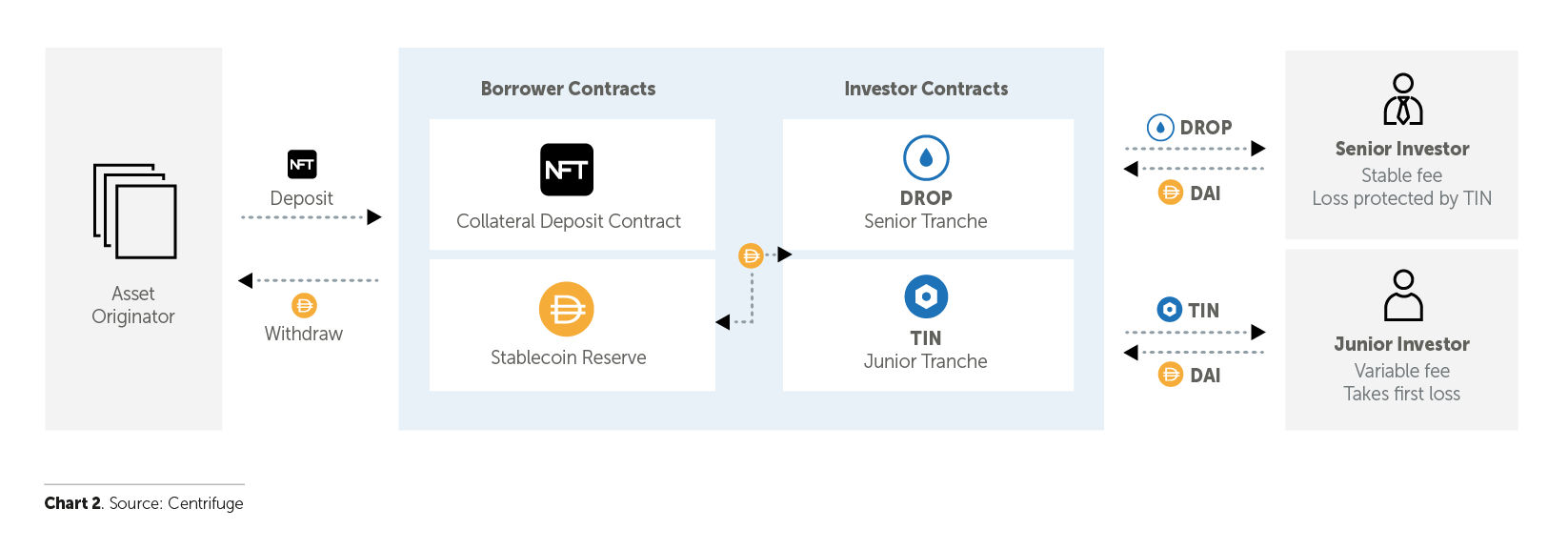

The platform connects investors and asset originators, who can borrow against their real-world assets. These real-world assets can be locked as collateral in so-called liquidity pools. Investors provide funding to the liquidity pools and finance the assets locked in them. The asset originator can borrow funds from the investor against the locked collateral.In this way companies can finance their capital needs either directly onTinlake, acting either directly as asset originators or indirectly by partnering with a particular asset originator such as New Silver, 1754 Factory, or Consol Freight, who then acts as an intermediary.

An investor can finance loans by investing in two different types of tokens: (1) The DROP token represents a lower-risk senior tranche that bears a fixed but lower yield. (2) The TIN token represents a riskier junior tranche that bears a higher but variable yield. If an asset is not repaid, TIN token investors are the first to take a loss. Every pool is specific, but usually between 8 % – 20 % of the value of underlying assets must default before a DROP investor sees any loss.

Every pool has a predefined minimum buffer value that, if reached, will trigger the protocol to close the pool to new investments in the senior tranche and let investors enter only the junior tranche. The amount of TIN issued in each pool affects the yield distributed to TIN investors, and the size of the pool is controlled by the asset originators. The buffer value is set based on the risk characteristics of the underlying asset types. New asset originators are also required to invest up to 50 % of the total amount in the junior tranche (TIN tokens) to align incentives. As time passes and the asset originators gain reputation, this value could decrease to 25 %.

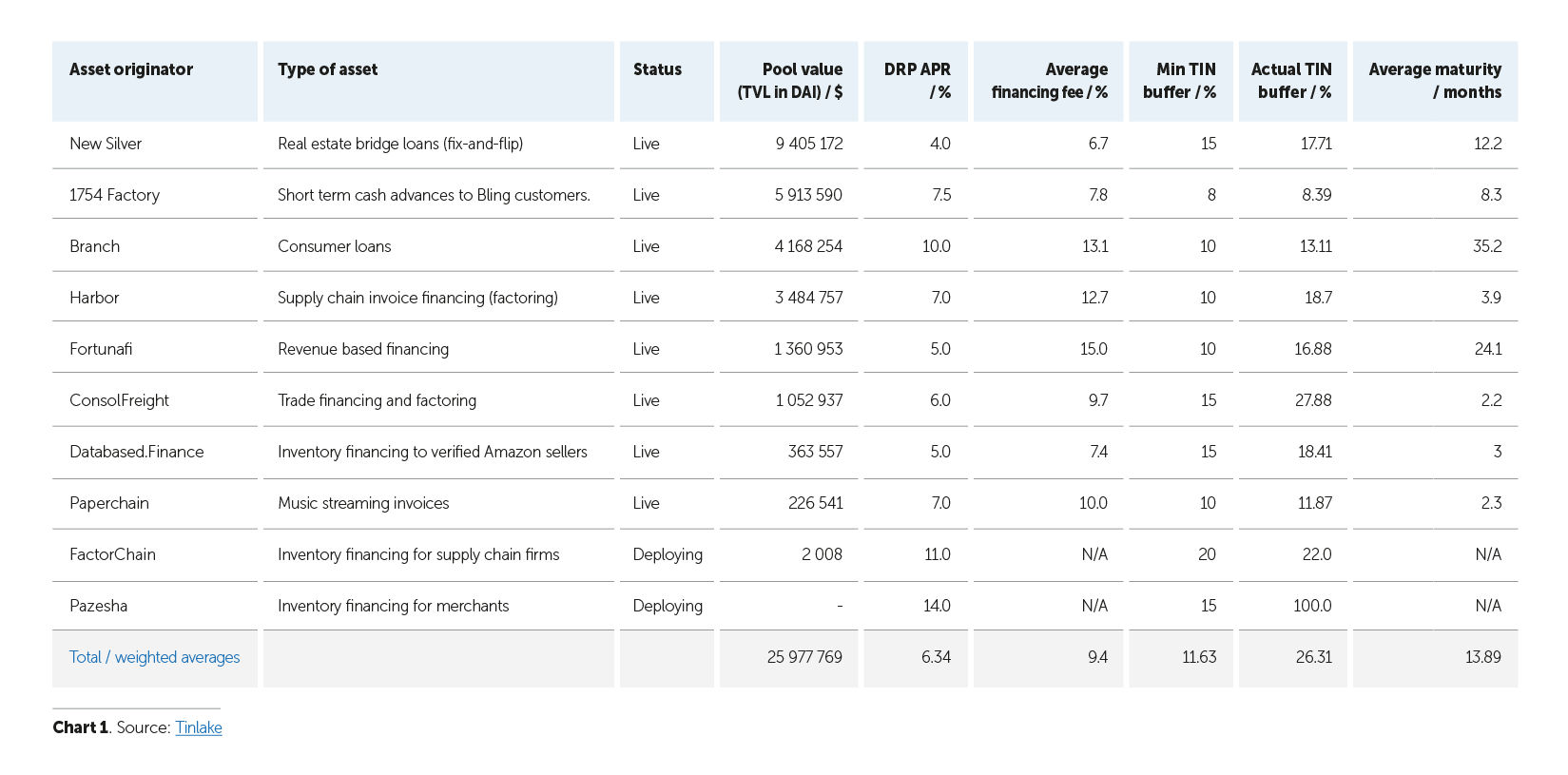

The details of assets financed through the pools differ greatly. For example, New Silver Series 2 finances “fix and flip” real estate loans with an average maturity of 12.2 months and a senior tranche yield of 4 %, while 1754 Factory finances short-term cash advances with an average maturity of 8.3 months and a senior tranche yield of 7.5 %. Other assets financed via Tinlake include working capital (invoices) expenditures (Harbor Trade, Consol Freight), advance inventory purchases for proven Amazon Sellers (Databased Finance), or advance payments for artists and media companies so they can access their streaming revenue much earlier than they could otherwise. See the summary in Chart 1 below.

Chart 2 below outlines the relationship between asset originators and DROP and TIN investors. A good Centrifuge and Tinlake explanatory video is available here.

Chart 2 below outlines the relationship between asset originators and DROP and TIN investors. A good Centrifuge and Tinlake explanatory video is available here.

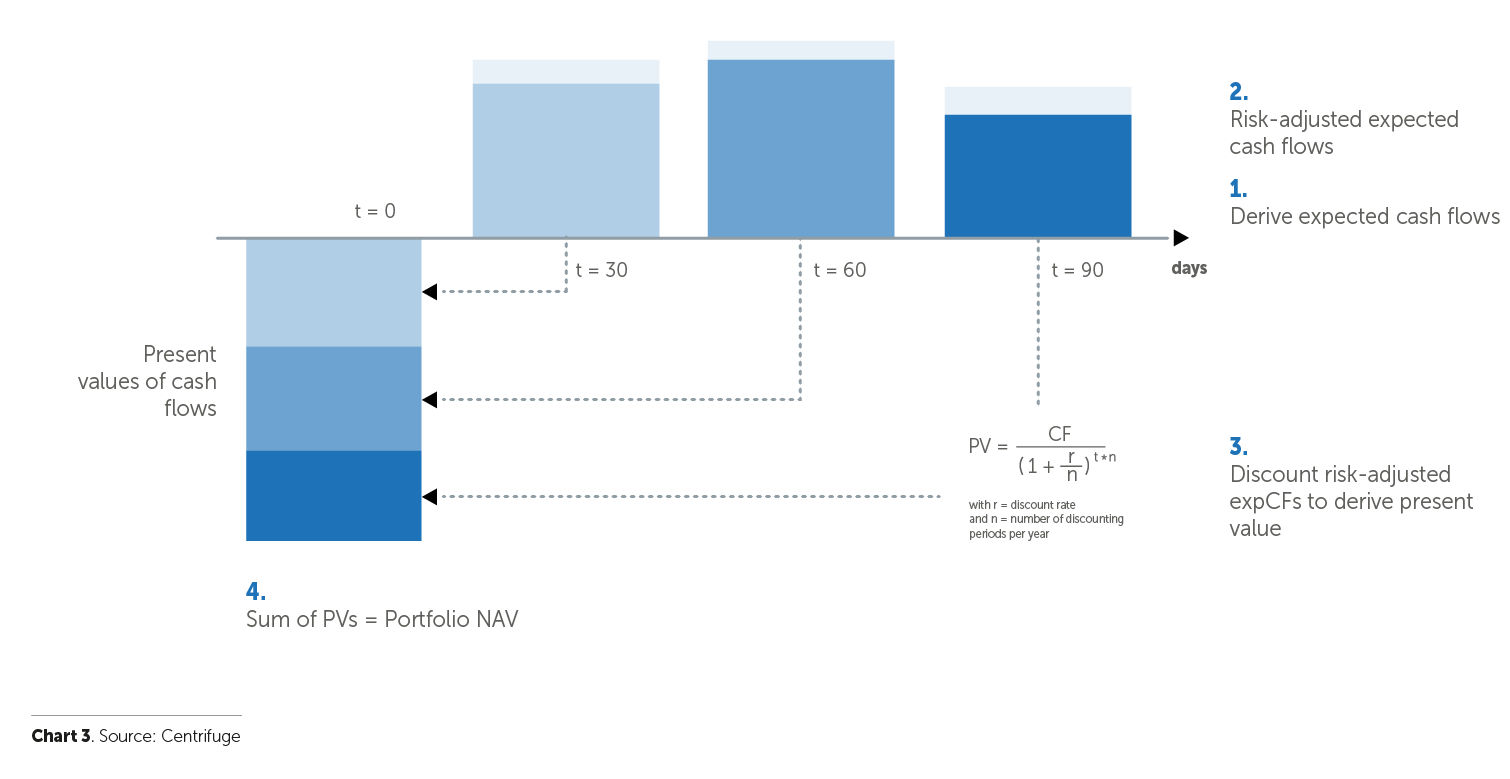

Investors in both tranches can invest in and redeem DROP and TIN tokens each time a new epoch starts, which is usually every 24 hours. At the end of every epoch, a smart contract calculates the NAV of the pool and accrued interest for investors. A good description of the entire process at the end of each epoch is provided in the documentation. The valuation method used is the standard DFC model and can be reviewed here (Chart 3). At this newly specified price, new and old investors can invest and redeem their tokens.

REVENUE

Revenue on the Centrifuge blockchain will be generated mostly by originating new fixed income securities. Whenever a new loan is financed from the pool, the protocol takes 30bp fees. The fee is taken in the underlying currency (DAI), which is converted into CFG tokens in the open market. A portion of the newly collected CFG tokens is burned (buy-back and burn program), and the remainder goes into the Centrifuge Treasury, which is controlled by the CFG token holders. The exact proportion will be set by a governance mechanism.Tinlake also plans to implement a flat fee on various types of transactions such as repayment fees ($0.40 per transaction), underwriter fees ($0.75 per transaction), investment fees and redemption fees (both $0.20 per transaction). These fees will likely be small relative to revenue collected from asset origination and the specific amount might be different when finally implemented. Other fees might also be implemented in the future as the functionality of Tinlake expands. In the future, Centrifuge might develop other applications that will generate cash flow. One possible vertical for expansion is development of its own money market like Aave and Compound. Our valuation does not consider other possible revenues apart from revenue generated on the Tinlake platform.

USP

Financing via Tinlake has several advantages for the asset originator in comparison to obtaining financing via an investment bank. First, after the initial pool is set up, the process is simple and does not require many administrative resources to draw capital. Second, capital can be obtained faster and on a couple of days’ notice. Currently, there is an excess of capital in the DeFi space that is looking for yield, and asset originators can leverage current market conditions. Faster access to capital helps the asset originators decrease working capital requirements, thus making their operation more efficient. Also, financing via Tinlake can be cheaper for some asset originators than financing their assets via investment banks. Finally, financing via Tinlake is accessible to more SMEs, which will otherwise not be financed, because they would be overlooked by banks.

Tokenomics

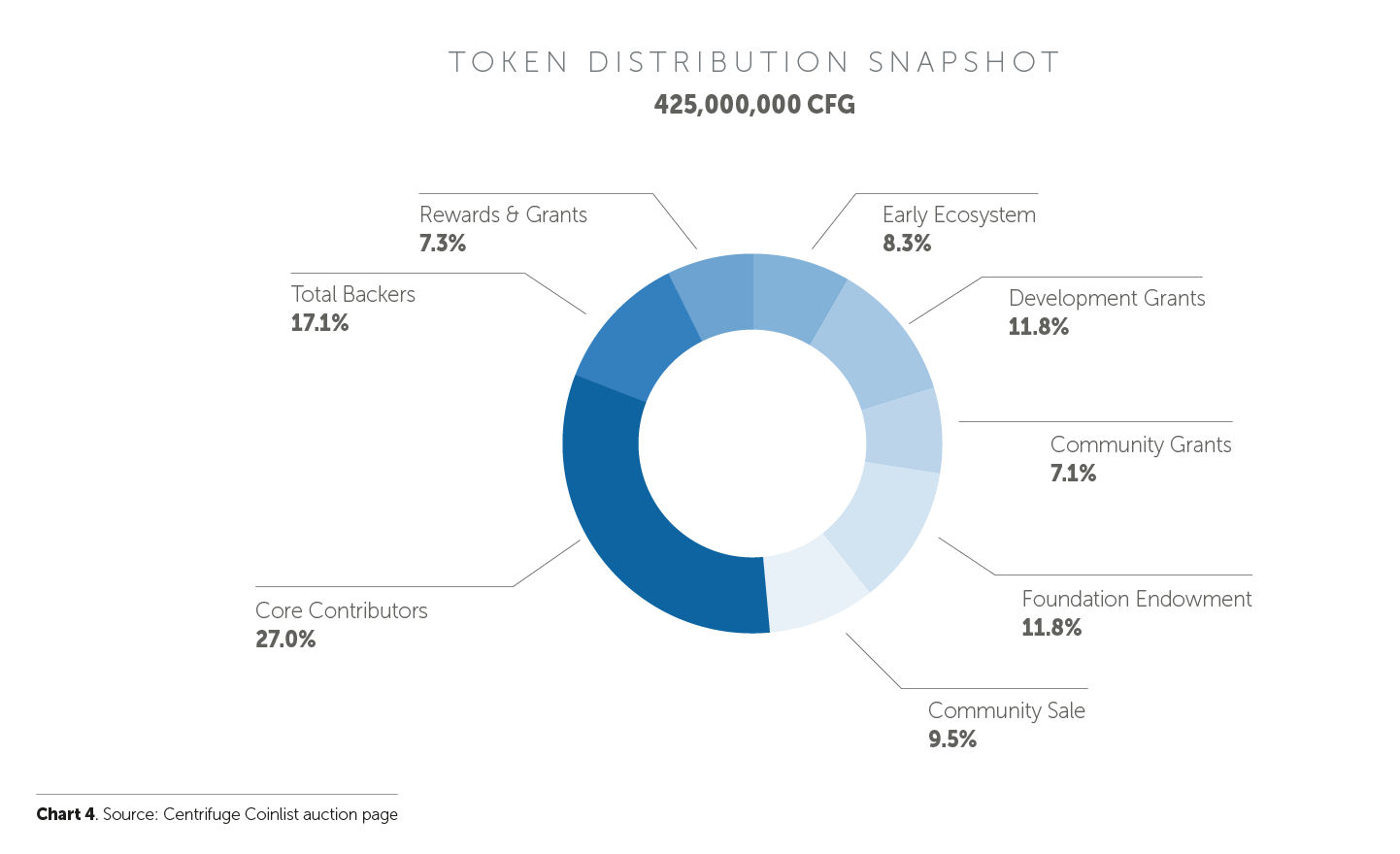

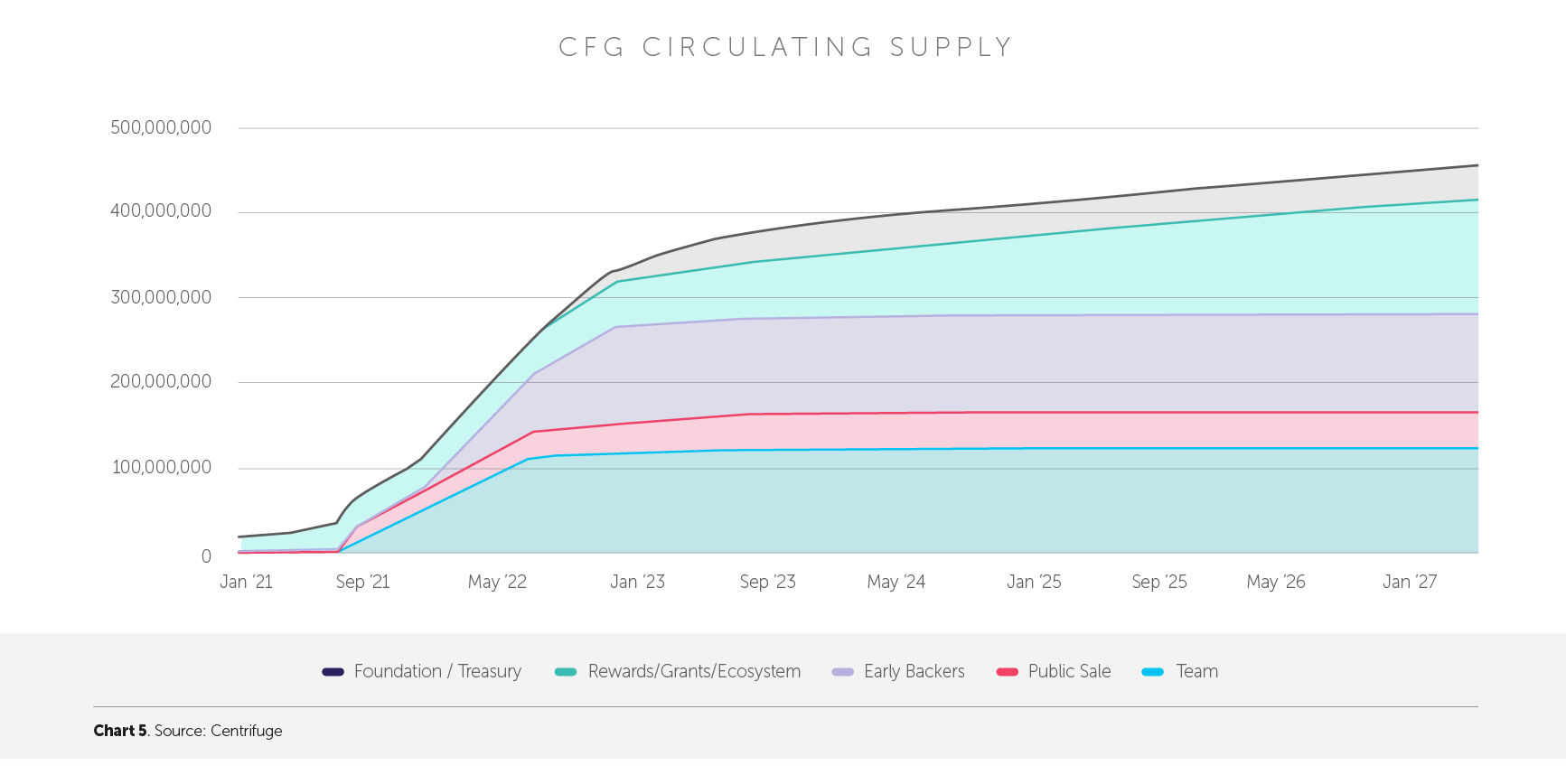

The Centrifuge token (CFG) is the native token of the Centrifuge blockchain living on Polkadot with a wrapped version on Ethereum. The token is a governance token that is also used for staking and paying transaction fees. There is a total of 425M CFG tokens distributed to stakeholders as shown below. In the short to medium term, the total supply will likely increase by 3 % p.a., but it is expected that the buy-back and burn program will stabilize the total supply at around 450M tokens over time. In the future, the parameter governing how many of the tokens are burned and how many go to the treasury will be set by governance voting.

The system pays Polkadot for chain security by issuing new tokens. The newly minted tokens will also be used to incentivize adoption of the platform by distributing CFG tokens to investors or asset originators in the Tinlake pools. On-chain governance voting can change parameters such as the distribution of newly minted CFG tokens as well as parameters of the Tinlake platform like risk models, liquidity provisions, and reputation mechanics.

Team allocation is approximately 27 %, with their tokens being subject to a lock-up schedule. Lock-up of the core team is set to a reasonable 48 months with a 12-month cliff. The release for the core team will start in July 2021. Core contributors have a shorter 1-year lock-up with no cliff and their tokens will start releasing in July 2021.

Tokens of the early-stage investors will start unlocking in December 2021 and will unlock over a 1-year period. Rewards distributed to protocol users have no lock-up. The Chart 5 below summarizes the expected release of the tokens.

Overall, token distribution seems to be fair, with all parties having significant exposure to the success of the platform. Token functionality and the release schedule are well-designed and create good value alignment between early investors, the team, and platform users.

The Centrifuge blockchain leverages security from the Polkadot blockchain. In comparison to a separate blockchain solution, Centrifuge expects to pay less for security and thus will have more resources to invest in growing the platform.

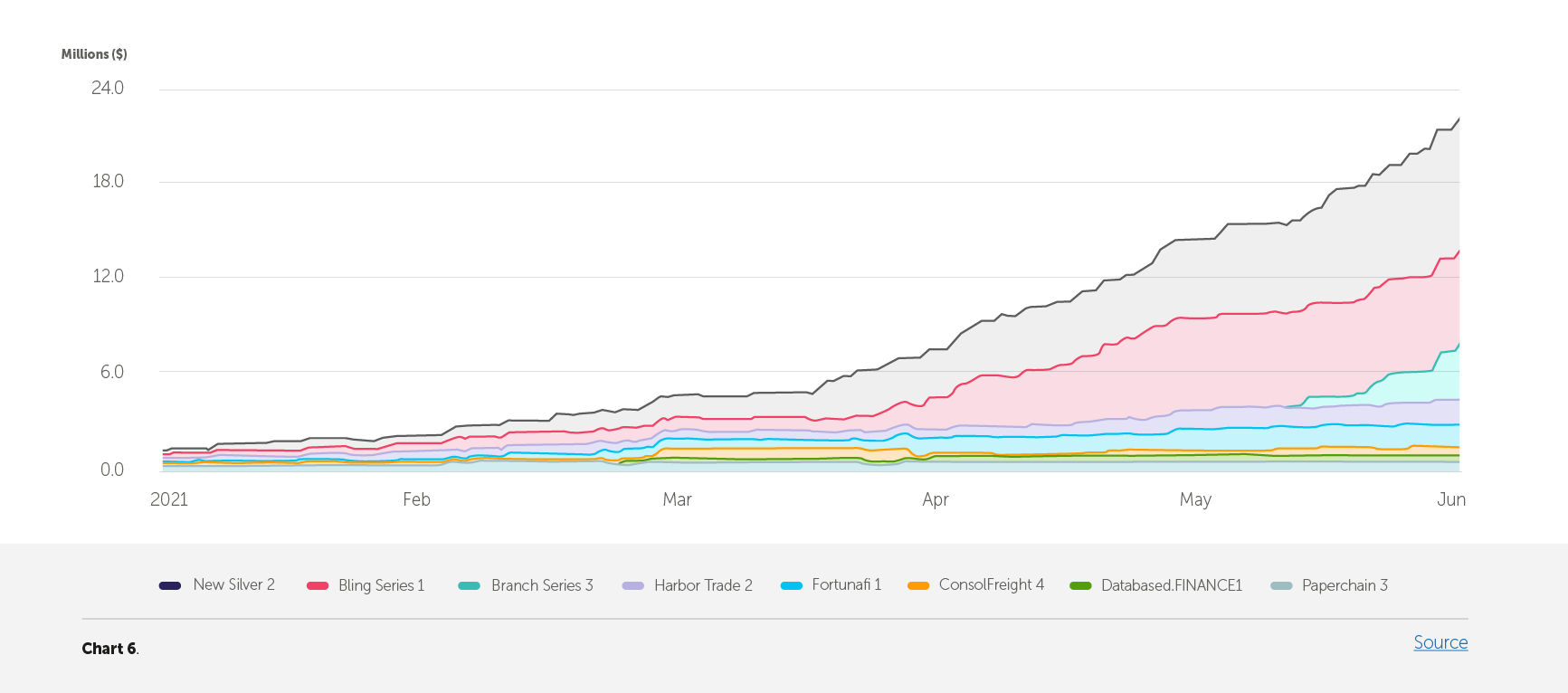

Traction

The total value locked in the pools has been growing at 73 % CMGR from the end of October 2020 to June 2021. The current growth is driven by expanding the value financed through the pools that have already been deployed. By early July 2021, there were ten pools, six of which were oversubscribed. There was a total of approximately 26Mlocked total value (TVL). The growth of the TVL can be seen in Chart 6 below. Among the largest pools are 1754 Factory, with $5.9M locked-in financing, and New Silver Series 2, with approximately $9.4M locked-in financing.

We expect Tinlake to gain even more traction, with potentially up to 2-3 new pools being live by the end of 2021. By the end of the year 2021, we also expect approximately $445M in total value locked and $186M in new monthly originations. The growth of the Tinlake platform is a chicken-or-egg problem. On the one hand, the platform needs pools with sufficient capacity of assets to be financed. On the other hand, sufficient investors are needed to invest enough capital in those assets.

This balance changes frequently and is not easy to strike and maintain. It is likely that Tinlake will not grow at the optimal rate due to either the demand or supply side slowing growth. However, based on the recent community call #14 (19:22 – 26:30), Tinlake enters into conversations with large asset originators that might be interested inlaunching pools $100M+ in size. Tinlake is also increasingly targeting institutional investors to increase originations via Tinlake. Institutional investors have access to greater capital than retail investors and canhelp grow Tinlake faster and more reliably.

THE TEAM

The Broader Team

Key people working for Centrifuge include Cassidy Daly (LinkedIn), Michael Ruzic-Gauthier (LinkedIn), Dennis Wellmann (LinkedIn), Miguel Hervás (LinkedIn), Alina Sinelnikova (LinkedIn) and Colin Cunningham (LinkedIn). The broader team has entrepreneurship experience from Chlu; VC and finance experience from BMO Capital Markets, NetScientific Group and Berenberg; engineering experience from Stellar, SatoshiPay, and Taulia; and research and academic experience from Macquarie University. The individuals working on the Centrifuge network are well educated, have a complementary skillset, and are experienced enough to propel the project forward.

Investors

Centrifuge is backed by top traditional and crypto VC investors. Centrifuge raised a $8M seed round in Q1 2018 from Blue Yard, Atlantic Labs, and others. Later, in 2020, the project raised a $4.3M round from mostly crypto-first investors like Rockaway Blockchain, Fabric Ventures, and Fenbushi Capital. At the end of May 2021, Centrifuge raised $19M in a Coinlist auction by selling 42.5M CFG tokens. Centrifuge is therefore well-capitalized to accelerate growth in the near future. A total of 11.8 % of all tokens is allocated to the Centrifuge foundation to ensure the project’s long-term sustainability. The treasury holds more than enough tokens to secure operation of the project for at least3-4 years, possibly even longer.

Partnerships

Centrifuge has established at least two key partnerships, one with Aave and one with MakerDAO. Partnership with MakerDAO enables the assets from Tinlake to act as collateral in a MakerDAO smart contract. Maker will provide capital against Tinlake pools and act as a decentralized source of capital. In other words, Maker will lock real-world assets as collateral in its smart contract and will mint DAI that will be paid out to the asset originator such as New Silver. There is a limit on how much capital Maker can provide. Looking at one already live integration of Maker and New Silver Tinlake pool, this limit is currently set at 5M DAI. Currently, 4.5M DAI has been financed via Maker and integration with the New Silver pool has been live since end of April 2021. There will likely be additional integrations with other asset originators in the future, but at present only integration with New Silver is live.

Centrifuge is also working with Aave to bring real-world assets to DeFi (source). Under the proposal, Aave users will be able to provide capital directly into Centrifuge’s pools within the newly planned permissioned Aave protocol. In this way, Aave users could gain a relatively stable yield generated from real-world assets, while asset originators can gain access to more capital distributed across the Aave user base. Aave token holders will decide under what risk parameters the Tinlake pools will be integrated into Aave. More detailed description of the partnership between Centrifuge and Aave is available here.

Deep integrations of Tinlake’s pools with DeFi protocols such as MakerDAO and Aave will place Tinlake at a first mover advantage when it comes to financing real-world assets through DeFi protocols. Integration of DeFi protocols like Maker stabilizes the supply of capital to asset originators, allowing them to operate with a higher degree of certainty. As the market expands, so should the integrations, which will accelerate Tinlake TVL and new loan originations.

Community

The Centrifuge community received a significant boost from the Coinlist auction. Twitter followers increased from 10.9k at the end of April to 26.8k (+146 %) by the end of May. On a similar note, Telegram members increased from 2.8k to 11.8k (+296 %) over the same period. A strong community is an important aspect that helps with word-of-mouth marketing. A strong and large community can easily bootstrap network effects and, for example, persuade other communities to vote for Tinlake’s integration into other DeFi protocols. Centrifuge can also, for example, rely on crowdsourcing feedback and thus get valuable customer information for improving the platform.

Market

From a broad perspective, Tinlake operates in two large markets: asset-backed securities and invoice factoring. Like Uber, which doesn’t operate its own taxis, Tinlake as such doesn’t underwrite loans, relying instead on an established market of non-bank asset originators. These asset originators provide loans to their customers and temporarily put the new loans on their balance sheet as assets. The cash that is lent out comes from the asset originator’s limited working capital resources. Since these asset originators do not have a full banking license, they must refinance these loans by selling them to a financial institution. This process is called securitization, and consist of the asset originator bundling numerous loans into one security and selling the portfolio of loan contracts, usually called MBS, CDO, CMO etc.and collectively known as asset-backed securities (ABS), to large financial institutions like banks or pension funds.Any type of assets-backed loan can be financed via Tinlake. It depends only on the specialization of the asset originators and their willingness to finance the assets via Tinlake instead of a large financial institution.

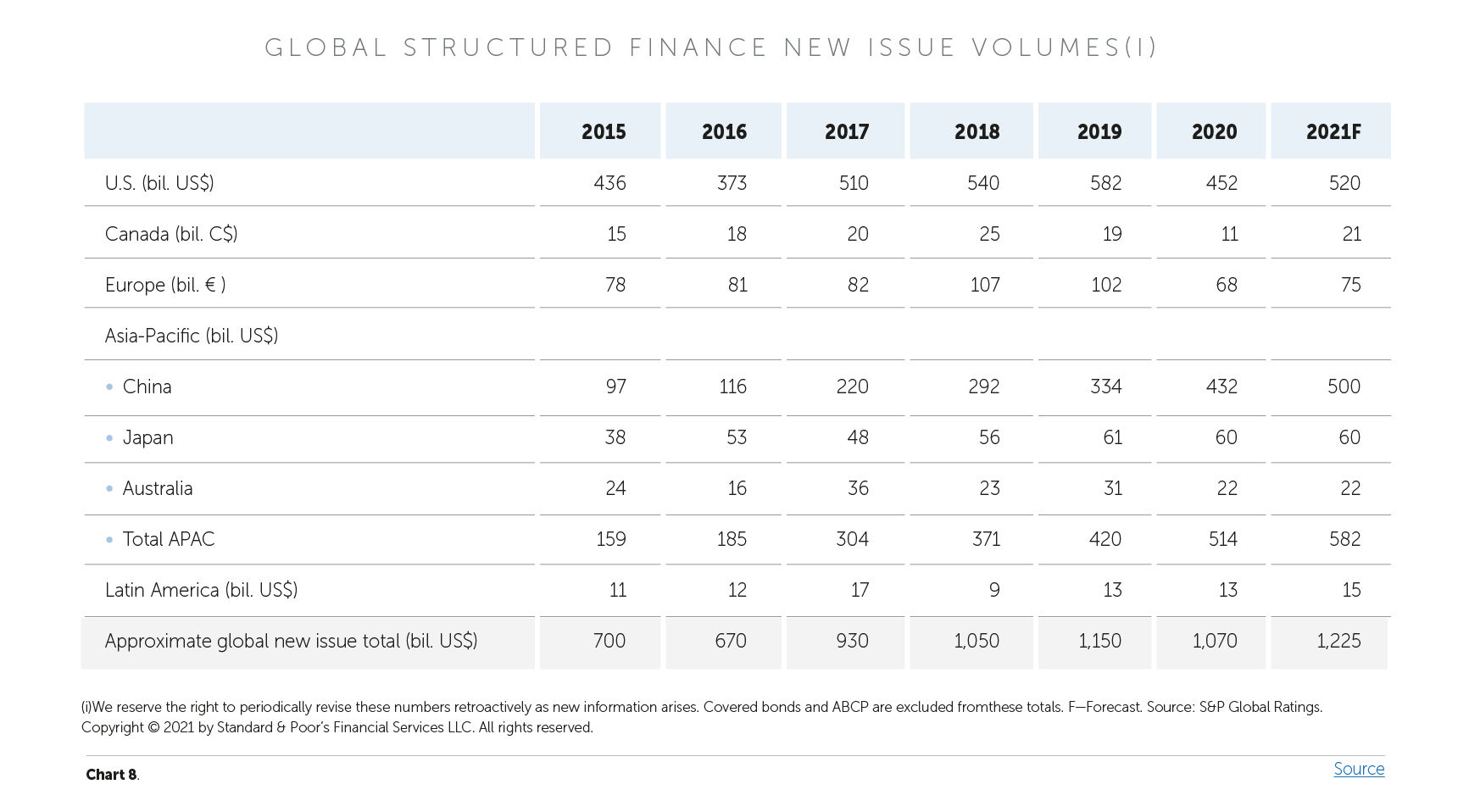

The total global amount of asset-backed loans originated is measured in trillions of dollars. According to S&P Global, $1.070T in total new asset-backed securities were issued in 2020, and this number is expected to reach $1.225T in 2021 (see Chart 8). Based on the 9.78 % CAGR between 2015 and 2021 and extrapolating the growth rate tothe next 5 years, we estimate new issues in 2026 to be worth $2.046T. If Tinlake is successful, it can achieve 3 % of the global ABS market, resulting in $61.3B in new securities being financed via Tinlake every year.

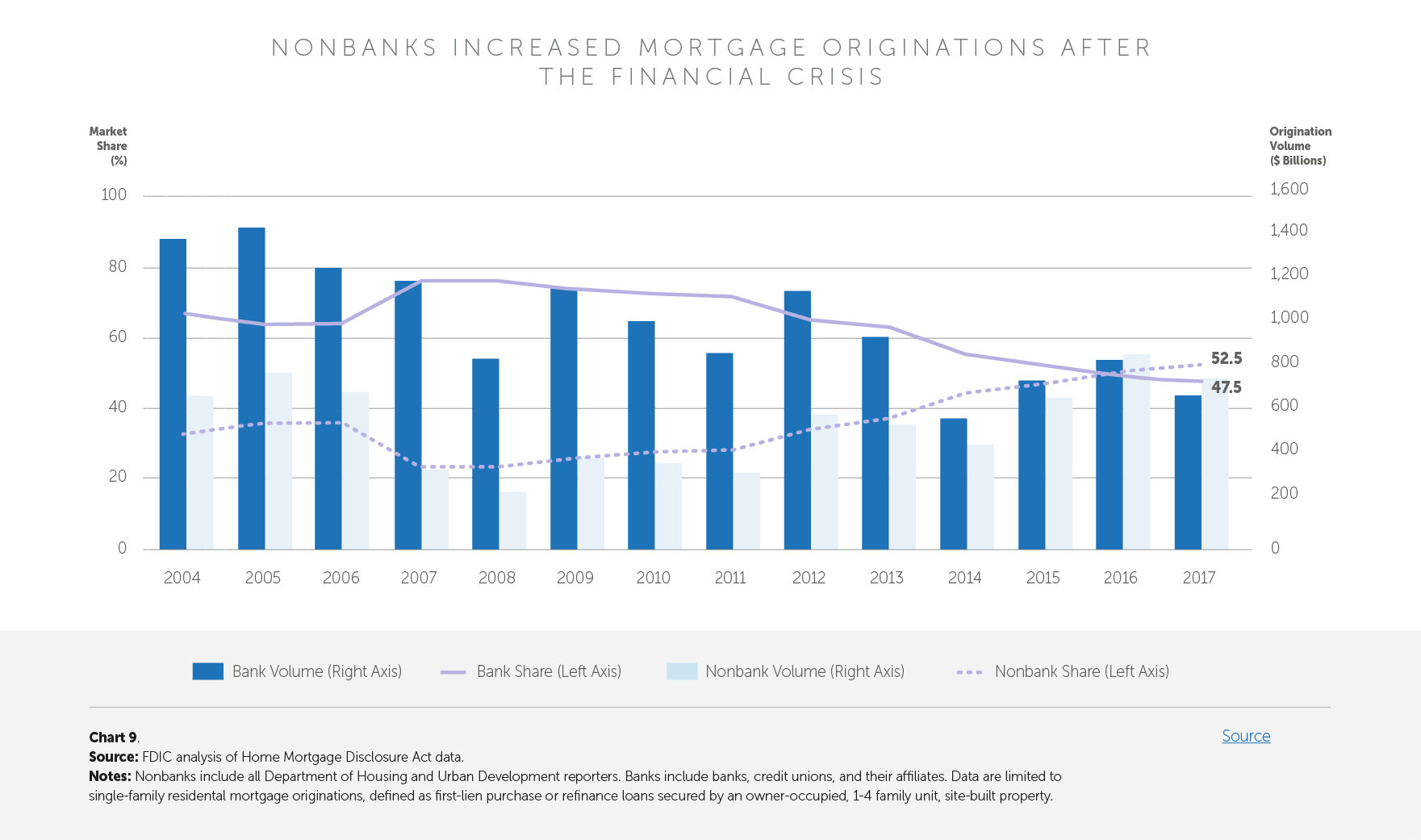

If we look more closely at one of the largest subsectors – mortgages, in 2017 in the USA alone, non-bank financial institutions providedmortgages worth $700B (see Chart 9). These nonbank mortgages are usually securitized and sold to financial institutions.

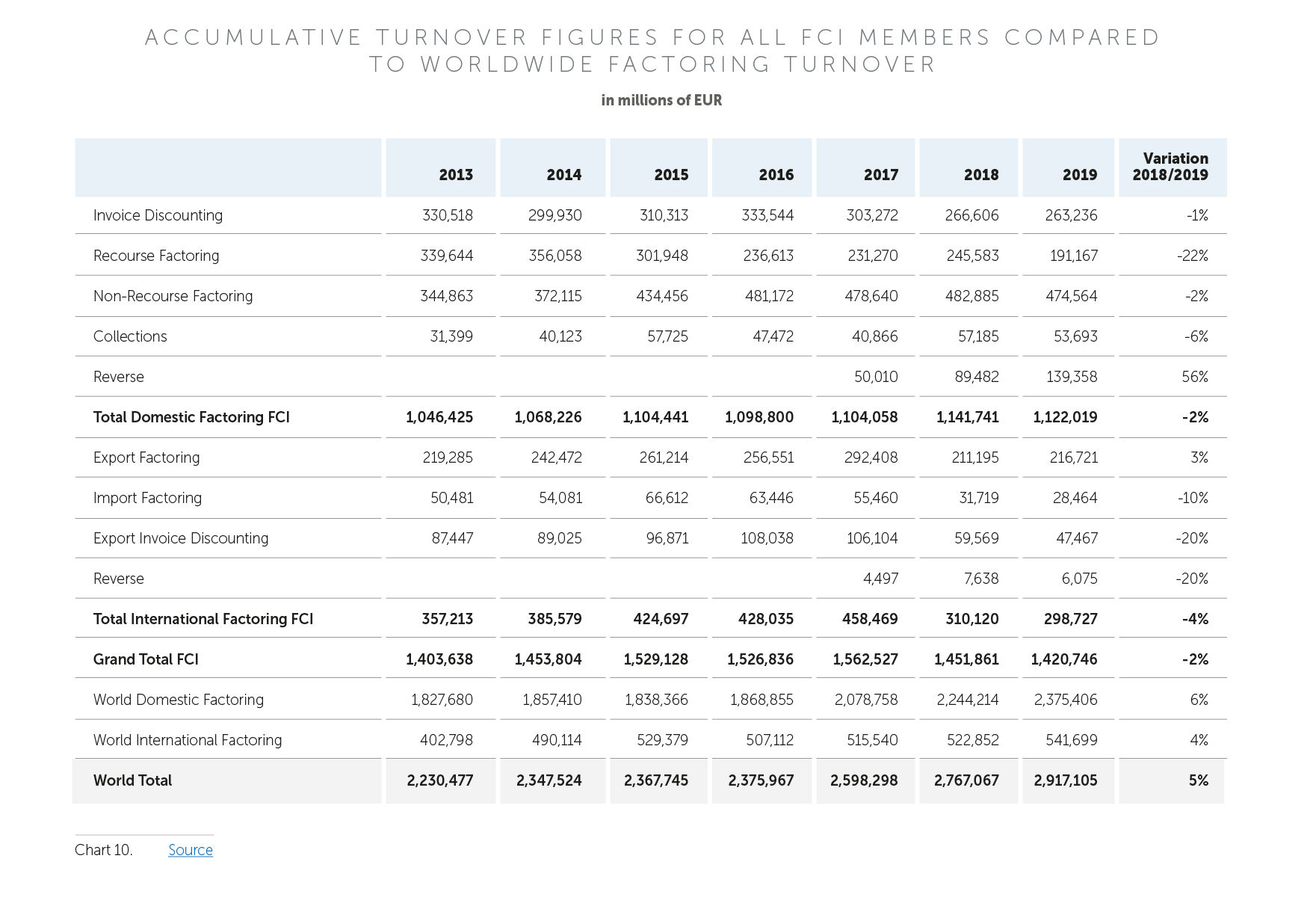

Another important loan type that asset originators finance via Tinlake is invoice financing services (factoring). Europe is the largest market for factoring, with its size estimated at €1.9T in 2019 (FCI 2020 report). In the same year, the value of invoices financed in the global factoring market was estimated at €2.9T ($3.5T) – (see Chart 10 for EUR values). Based on the 4.47 % CAGR between 2013 and 2019 and extrapolating the growth rate to the next years, we estimate the factoring market 2026 to be worth €3.9T ($4.7T). We expect that if Tinlake evolves into the go-to platform for asset originators and investors, it can also achieve €72B ($86B) in annual originations from the factoring vertical. This would translate into an approximate 1.8 % market share of the global factoring market.

On Tinlake, Harbor and ConsolFreight focus on financing working capital (payable invoices) for businesses in the supply chain industry. Harbor Trade currently has $3.5M locked in these assets and ConsolFreight approximately $1.1M.

Other loan types

There are also innovative loan types that are being financed via Tinlake. For example, an artist can get a loan collateralized by future revenue from Spotify, YouTube, Instagram, or other influencer-like business model revenue. For example, a Tinlake pool called Paperchain focuses on forwarding future Spotify revenue. To date, they have financed $230k. The size of such niche markets is rather small in comparison to securitized financial assets like mortgage financing, consumer loans, and corporate credits, but they provide an apt illustration of how almost any type of asset can be financed via Tinlake.

Competition

Bridging real-world assets to DeFi is not an easy task with a quick upside. Any company that interacts with real-world assets requires regulatory compliance. One such company that targets a similar market is Figure with its Provenance 2.0. blockchain. Figure originally started as an asset originator providing HELOC financing. There are several more companies focusing on bridging real-world assets to DeFi, such as Persistance, Tradeshift, and Fludity.

From a more traditional finance perspective, the competition comes from established investment banks that strive to securitize assets, like J.P. Morgan and Goldman Sachs. To gain an edge against these established financial institutions, Tinlake must be more competitive in terms of process, capital efficiency and timeliness when dealingwith asset originators.

Valuation

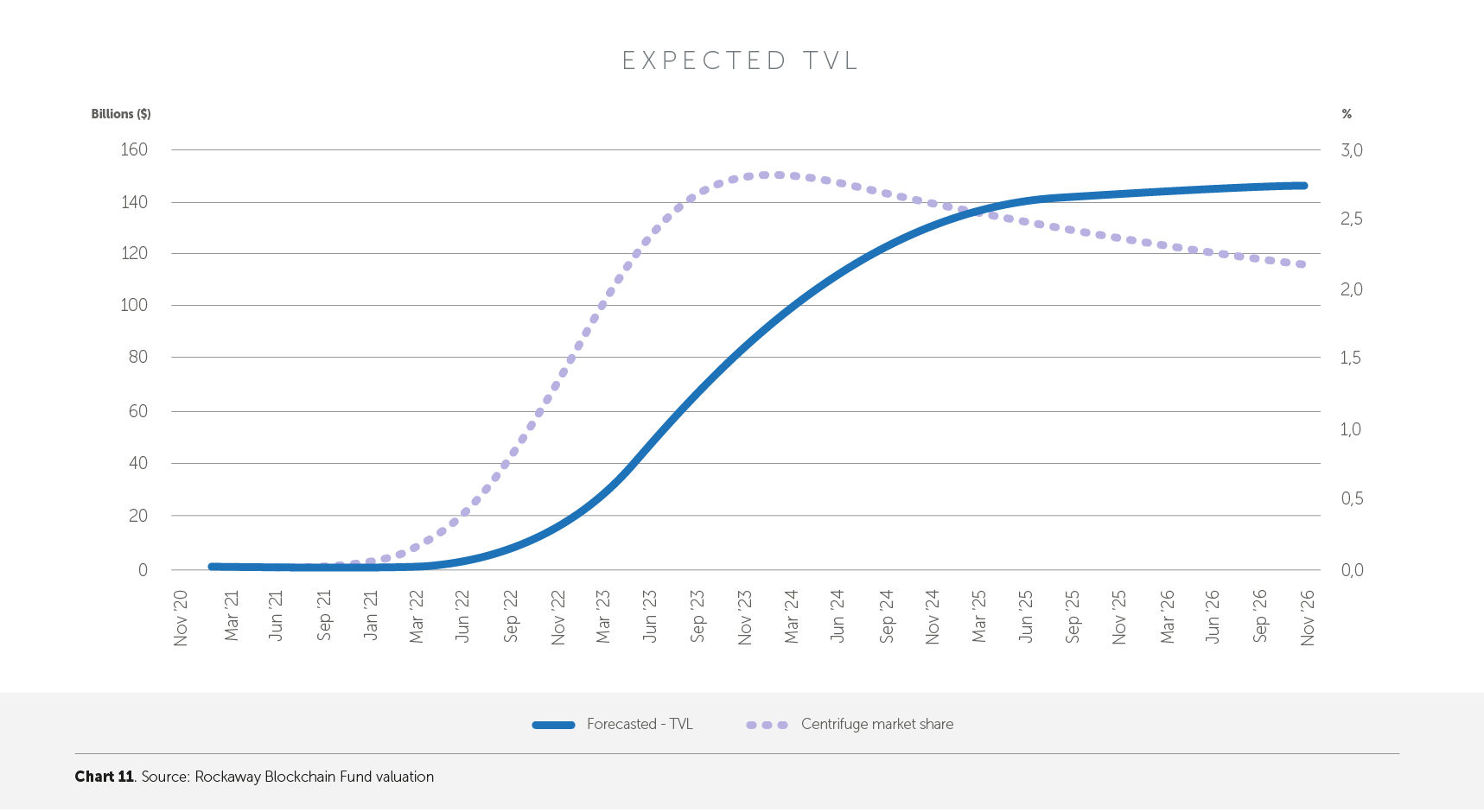

Tinlake has been growing at an average monthly rate of 73 % since October 2020. For comparison, the broader DeFi market as measured by DefiPulse TVL has been growing at 27.4 % since January 2020. We expect that Tinlake can grow at a 15.5 % average monthly growth rate until the end of 2026. If Tinlake maintains our projected traction and becomes successful, we expect it can originate $148B in new loans every year and achieve approximately the same amount in TVL by the end of 2026. This would result in gaining approximately 2.2 % of the combined securitization and factoring market. See Chart 11 below for TVL and market share projections. Such numbers mean that Tinlake’s growth will depend on mainstream adoption of DeFi and on whether and how fast blockchain protocols look for integration with real-worldassets.

The current average maturity of loans originated via Tinlake is approximately 13-14 months. We do not expect that the average maturity of all loans originated via Tinlake will change significantly in the future. Based on management expectations, in our model we projected average maturity at 12 months. A shorter average maturity is preferable, because Tinlake generates 30bp on every new origination. We do not expect large downward pressure on the 30bp fees during the 5-year investment horizon, as traditional businesses have barely tapped the market potential of DeFi and will probably rush to gain access to DeFi services during this period. The demand for DeFi financing from real-world asset originators will likely keep the demand for Tinlake services high. We expect Tinlake to evolve into the market leader in providing real-world asset-backed loans financed by capital coming from digital assets. By the end of 2026, we expect $37M monthly revenue from asset origination with $12.3B per month in new loan originations from 82k monthly transactions.

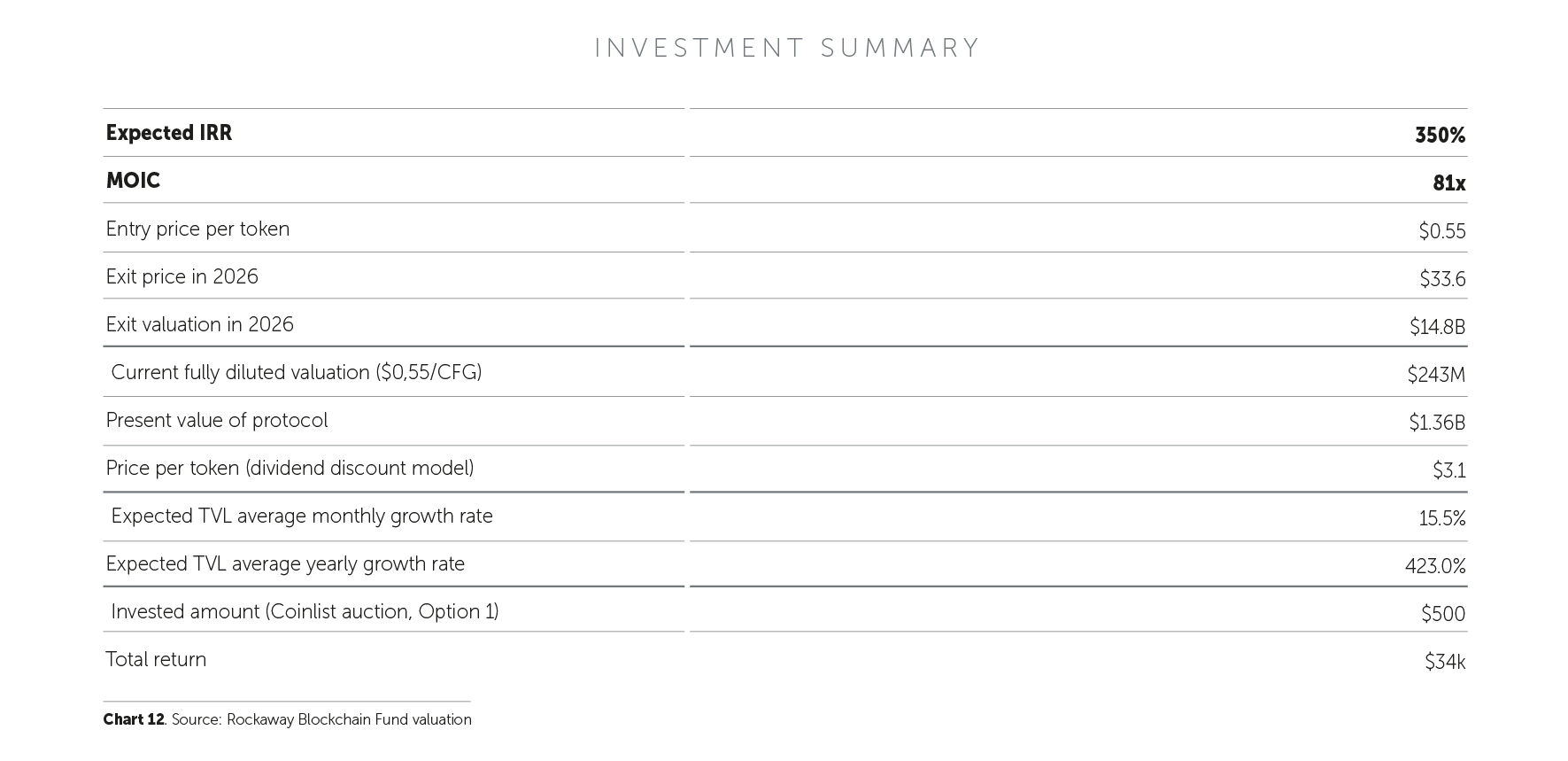

Currently, the main purchasers of ABS are pension funds, banks, and insurance companies. We expect a shift away from retail users to institutions as the main customers for Tinlake. Financial institutions will invest higher tickets and hold the assets on their balance sheet. Such a shift can be accelerated by a clear regulatory environment.Based on the stage of the project, we used a 60 % discount rate. Our model shows a PV of $1.36B or $3.1/CFG token. At the end of the investment horizon (December 2026), we applied a 0.1x Price/Origination multiple to annual revenue.

We estimated the 0.1x Price/Origination ratio based on publicly traded Lending Club (NYSE: LC) 2020 originations and its current market capitalization. As such, we project ending fully diluted CFG valuation at $14.8B or $33.6 per CFG token. Our new price target for the CFG token is therefore $33, and we expect it might achieve this target at some point by the end of 2026. Such an increase would yield an investor that purchased the token for $0.55 a multiple of 81x on the investment and distributed cash flow over the period of next 5 years.The corresponding IRR is 350 % over the same period. See the summary in the Chart 12 below. If you are interested in the details of the valuation model, feel free to contact us (Twitter @RBF_cap, or @DavidRakusan).

Risk

BUSINESS MODEL

In the short term, Tinlake’s business model is susceptible to a mismatch between demand and supply for financing. At present the demand side is driven by business development and the need to strike partnerships with real-world businesses and persuade them to access financing via Tinlake. On the other hand, the supply side is driven by the demand for yield from the Tinlake community and other DeFi protocols like Aave and Maker. In the short term, Tinlake business developers might have a hard time closing deals with real-world financial institutions if most of them don’t trust DeFi.The short-term growth rate might thus be limited by the new partnerships closed by the business development team. In other words, the market might not be ready for widespread DeFi adoption. However, we believe that in the long term most institutions will see the benefits of DeFi and will eventually look for financing methods via DeFi.Interested companies will be able to tap into Tinlake’s financing without the need for any interaction by the Tinlake business development team.

REGULATORY

The adoption of Tinlake is also influenced by the regulatory environment. Asset originators will be more attracted to leverage the efficiencies of Tinlake if they see established, stable, and predictable regulation. The faster regulation arrives the better for Tinlake, because this will lower barriers for institutions to implement Tinlake. If, on the other hand, regulation doesn’t arrive at all until the end of our investment horizon, Tinlake might lag behind our projected adoption from asset originators.

SECURITY

As is the case with every protocol, Tinlake can also face some security issues. In the event of some smart contract vulnerability, the funds in the individual pools might be at risk. This risk is mitigated by smart contract audits. Tinlake code has been audited by Trail of Bits and Least Authority.

ASSET ORIGINATOR AND COLLATERAL RISK

An investor on Tinlake must trust the asset originator to originate loans (assets) with the same risk profile over a longer period of time. It is hard for the investor to verify what types of assets are being originated, as the investor doesn’t have access to complete information about the underlying assets. Currently, the role of underwriter is performed by asset originator. In the future, the roles of asset originator and underwriter should be split, thus partially mitigating this conflict of interest.

Conclusion

In conclusion, we see Centrifuge as a blockchain that will be on the forefront of real-world asset migration to blockchain. Tinlake is well positioned to evolve into a leading platform for structured fixed-income assets. We consider the team to be very experienced and believe they can create a best-in-class product that institutional investors will use extensively due to the increased capital efficiencies that Tinlake offers. If the regulatory environment evolves in the right direction, asset originators might adopt blockchain technologies at a faster paceand Tinlake can benefit from this environment. As such, we believe that the total value locked in securities financed via Tinlake will grow at an average monthly rate of 15.5 % (423 % annually) over the next 5 years and achieve $148B in new annual originations by the end of 2026.Finally, increasing total value locked and loan originations will translate into increased value of the CFG token, which can potentially reach $33 per token. If you are interested in the details of the valuation model, feel free to contact us (Twitter: @RBF_cap, or @DavidRakusan).

Disclaimer

This article is for informational purposes only; it is not investment advice and we disclaim any and all liability for the information provided. It involves a number of assumptions, risks, uncertainties, and other statements; actual results may differ materially from such statements. No representation or warranty (expressed or implied) is made as to the fairness, accuracy, completeness, or correctness of the information provided or opinions contained in this article and nothing contained in this article should be relied upon as a promise, representation, or indication of the future performance of any asset. No information contained in this article constitutes an offer or invitation to purchase or subscribe to any interest in any asset and no part of it shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. Any logos and trademarks are displayed in this article for informational/educational purposes only and do not constitute any endorsement of any offering or any investment product.

David Rakusan is Investment Manager at Rockaway Blockchain Fund, responsible for portfolio management. He previously worked as an Investment Analyst at RSJ Investments, a financial group with €500M in assets under management, where he was responsible for analyzing both direct investment opportunities and indirect fund of funds investments in the VC sector. David holds a a Master’s Degree in Finance and Financial Management Services from the University of Birmingham and a CFA charter.