The metaverse, is it hype or reality?

McKinsey estimates the metaverse market will grow 130x from $38 billion in 2022 to $5 trillion by 2030. Citi’s estimate of the potential is even larger, at $11 trillion. And with Facebook renaming to Meta and allocating an annual budget of $10 billion to develop the metaverse, there has been an overwhelming discussion in the investor community on what the metaverse is and how to make money from it.

The usual definition of the metaverse is an immersive 3D world with triple A graphics. Interestingly, this remains close to a definition by Neal Stephenson, the author who coined the term in 1992 - an all-encompassing digital world that exists in parallel to the real world. Investors may think that the biggest upside lies in its gateways, the picks & shovels. While virtual reality (VR) and augmented reality (AR) headsets are not a small market, the largest upside comes from building blockchain-based open economies and facilitating economic activity within them. Citi estimates the VR headset market to reach 200-250 million units sold annually in 2030 ~ $150 billion, a fraction of the overall potential $11 trillion market.

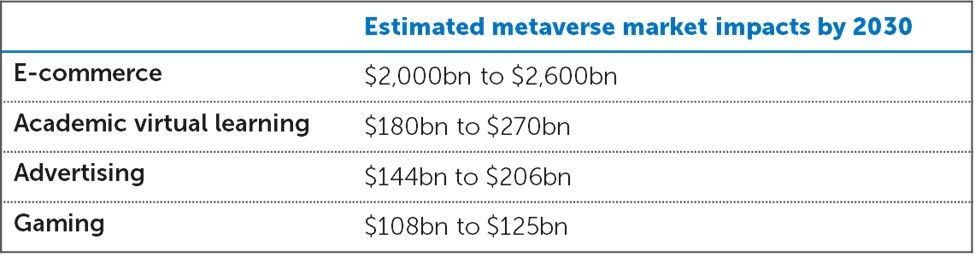

Considering the more conservative $5 trillion McKinsey estimate, metaverse-based e-commerce, virtual learning, advertising, and gaming will collectively account for more than half of the market. McKinsey expects the metaverse’s impact on e-commerce to be $2 to $2.6 trillion by 2030, followed by virtual learning adding $180 to $270 billion, impact on advertising of $144 to $206 billion, and impact on gaming in the range of $108 to $125 billion.

Sources: McKinsey’s “Value creation in the metaverse” report

Web 3, creator economy supercharged

Facilitating economic activity in virtual worlds is not a metaverse-specific concept. In Web 2, it’s called the creator economy. With growth of 390% per year since 2016 and a market size exceeding $100 billion in 2021, it’s already big.

While the 390% year-on-year growth is impressive, creator empowerment is non-existent. Wealth continues to accumulate in rent-seeking Web 2 monopolies at the expense of the creator. TikTok shares 50% of revenue from creator videos, YouTube shares only 45%, and Roblox, after all fees, shares only 29%. As the Web 2 tech giants grow and gain strength, creators and consumers alike are becoming victims of their success. The terms of service governing creator & platform relationships have reached predatory levels with tightening content ownership rights and even accessibility of the platforms themselves. In 2020, for example, Activision Blizzard updated their terms of service for Warcraft 3, which now requires users creating custom maps to give up any rights of ownership and intellectual property (IP) over these maps without any remuneration. In the Web 2 “everything-as-a-service” model, YouTube, Twitch, Twitter, Roblox and others make unilateral decisions to restrict digital asset ownership rights and exclude undesired creators on a daily basis (e.g. Twitter deciding to ban accounts based on political views, or if you are a Twitch fan, remember the unexplained permanent ban of one of the most famous Twitch accounts, Dr Disrespect, with over 5 million subscribers). Consumers are not safe either - in 2022, PayPal leaked a policy under which the platform at its sole discretion could seize $2,500 from a customer account if it believed the account owner has been spreading misinformation (note that due to community backlash, PayPal soon after the announcement reversed its decision, and later re-introduced the same terms after the storm passed).

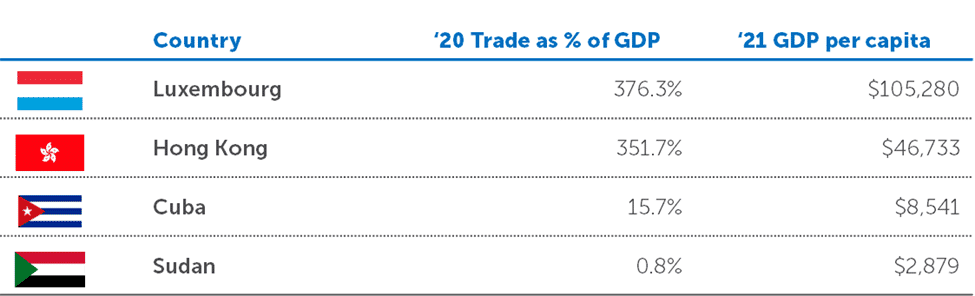

While Web 2 companies are built as closed platform economies, the highest-performing economies are open, with free access to services, trade and asset ownership. Drawing a parallel from the physical world, it comes as no surprise that the world’s most open economies (measured by total trade as a percentage of GDP) such as Luxembourg ($105,280) and Hong Kong ($46,733) exhibit on average 20x higher GDP per capita than the world’s most closed economies of Cuba ($8,541) or Sudan ($2,879). Putting this back in the context of Web 2, when thinking about the commonalities of closed economies such as government power, tight population control, and limited access to asset ownership, Twitch, YouTube, and other traditional creator platforms deeply resemble the economies of Cuba and Sudan.

Sources: https://ourworldindata.org/grapher/trade-as-share-of-gdp?country=ALB~North+America~NER, https://www.worldometers.info/gdp/gdp-by-country/

In our view, the structure of closed economies as implemented by the tech giants with monopolistic behavior makes the Web 2 creator economy ready for disruption.

The time is now!

In Web 2, custody of digital assets remains with the issuing platform, and ownership rights are tied to terms and conditions set by platform owners, which can change at a moment’s notice. And sometimes, such as in Marvel’s forced sales of IP rights in comic book heroes, even the ownership itself remains with the platform. Early Web 2 metaverses that are not operating on blockchain, such as Entropia or Second Life, are great examples of how much power companies have over their systems and how actions of these companies can lead to massive value destruction when they break the inherent trust in them. In 2007, Linden Labs, the company behind Second Life, decided to increase the rate at which Second Life digital land generates, accidentally causing the price of land to plummet by over 12% overnight.

For the first time in history, blockchain enables true ownership of digital assets. In contrast to Web 2, Web 3 assets are secured on the blockchain validated by hundreds or thousands of independent parties and cannot be restricted without consent of the creator or upfront predefined rules. There is no need for trust or an opportunity for monopolistic practices. On a blockchain, ownership of digital files is realized through NFTs. Simplified, NFTs are files that cannot be copied and are best used to store a record of ownership. Given the immutable properties, storing data on blockchain is not cheap (and currently ranges from $0.01 to $150 depending on the underlying blockchain and transaction complexity), so one has to assess the business model behind every write. As a consequence of true ownership, digital assets are able to accrue significant financial value. While large sales of digital assets in Web 2 are rare, NFTs worth thousands or millions of dollars are traded daily.

CryptoPunks, one of the most successful and oldest NFT collections, is a prime example of how valuable digital ownership can be. In 2022, CryptoPunk #5822 sold for $23.7 million, #7523 for $11.8 million, and in 2021 #4156 sold for $10.2 million. Early gaming NFTs are often selling for hundreds of thousands of dollars, with CryptoKitties’ Dragon leading the charts at a sale price of $172 thousand in 2018, followed by the Axie Angel sale price of $130 thousand in 2020, or God’s Unchained’s Hyperion sale price of $60 thousand in 2019.

With the maturing of blockchain technology, there is a solution that enables a persistent and immutable open economy where ownership rights are cryptographically guaranteed.

Current metaverse implementations show no traction, although the consumer demand is there

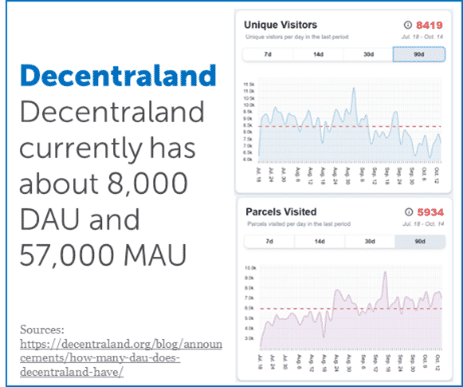

Current Web 3-enabled general metaverses lack traction, such as Sandbox and Decentraland, which are built as blank universes waiting to be filled and utilized by their owners. Both platforms exhibit less than 100 Daily Active Users based on observed on-chain activity, even if their creators claim it reaches single-digit thousands (i.e. 8,000 for Decentraland). The problem with general metaverses is that they don’t offer a clear purpose. They don’t solve any meaningful problem, and therefore nobody uses them.

The consumer demand for immersive virtual entertainment is visible. Concerts held in a virtual space by Justin Bieber, 21 Pilots, or Marshmello were each visited by over 10 million participants, while Ariana Grande’s performance attracted as many as 78 million fans. The reason why these success stories happened in Roblox and Fortnite and not a general metaverse is simple. Roblox has over 43 million daily active users and Fortnite is a close second with an estimated 25 million daily users. For the metaverses to gain traction, they need to find a beachhead market with a specific problem to solve. In the context of Fortnite and Roblox, it has been gaming and the creator economy.

The beachhead markets are gaming and work improvements

The work-related use cases for the metaverse are primarily focused on improving communication, collaboration, and work efficiency. Some early attempts to tackle these include:

- Meta’s universal speech translator that will be used in its metaverse for everyone to understand each other;

- SoWork’s, Meta’s Horizon Workrooms’, or Microsoft’s Mesh metaverse-based virtual collaboration spaces where employees can meet and engage in conversations or create multiple virtual computer screens without the need for physical devices; or

- Meta’s Quest Pro, a new VR set with eye tracking and improved virtual screen quality to boost metaverse work productivity.

Most of those solutions are still in development at the time of writing, but to compare with general metaverses, Meta’s Horizon World, and its Workrooms, is reportedly frequented by 200,000 users a month. Nonetheless, even as these use cases sound futuristic and exciting, we don’t think they are going to make it, as the “10x better” factor required to change human behavior is questionable. Initial research conducted by Coburg University in Germany actually shows that working in VR lowers productivity and can cause migraines. A survey of 1,500 employees conducted by ExpressVPN in 2022 showed that employees also worry about their employer’s ability to spy on them while working in the metaverse. None of these use cases can also leverage the open economy as there is no need for persistence of state.

On the other hand, we find the value proposition of social and entertainment-based metaverse use cases much more relevant. Storing the state of a game on blockchain enables new game economy designs and an undeletable trace of wallet behavior enables a composable and transferable digital identity. For example, a multiplayer tycoon game, Angry Dynomites Lab, aims to create a sustainable open economy where players work together to save the Dynos from extinction by collaboratively building powerful artifacts. In-game Dyno characters generate resources like fire, water, earth and air which can be combined into new items and new resources ultimately resulting in community-built artifacts called masterpieces. The game mechanics resemble Minecraft, though in a single world (stored on blockchain) and open economy setting which anyone can join and leave at any time. The business implications are three-fold:

- Independent creators can join and co-develop the Dyno world with their own content including new characters, new resources and side storylines. Similar to collaboration networks like Helium or Hivemapper, the business implication is a reduction of CAPEX as an exchange for equity.

- Game state and asset ownership records are stored immutably outside the control of game creator. A player’s actions permanently alter the world and cannot be rolled back, censored or otherwise restricted. Guarantees of digital continuity enable players to build in-game equity and result in high-value purchases and increased sense of belonging.

- Scarcity of resources and crafting recipes in an open economy setting allows items to accrue financial value and therefore enables the play-to-earn game mechanic as an adjacent business model to entertainment.

The business model of open economy games is still to be determined, but taxes & royalties receive the most support

While Web 2 giants generate billions of revenues from exploiting creators, charging 50% or more of revenue, Web 3-enabled companies with limited control over assets issued must find new ways to compete with Web 2. To be fair, the Web 3 open economy business model is still being explored, but we see early traction in secondary market royalties as well as discussions around continuous primary offerings and the Harberger tax system.

As asset ownership on blockchain is recorded through an NFT, the initial asset ownership transfer from creator to consumer occurs through a primary sale of this NFT, benefiting the creator. Because blockchain-based digital assets are persistent and based in an open economy, the initial consumer can resell them on a secondary market. In order to continuously recognize the original creator’s IP rights, a royalty rate initially set by the creator is charged on every secondary sale. Even though the royalty rates are usually fairly low (typically 5% to 15%), they can generate large returns for the creator over time. Yuga Labs’ collections, including its famous Bored Ape Yacht Club, generated almost $5 billion in lifetime secondary sales, which at a 5% creator royalty rate brought the company $240 million. To name a few more, the Doodles and Azuki collections each generated over $20 million in secondary royalties.

Despite the traction we see with this business model, there is an ongoing discussion regarding how sustainable royalties are since they may lead to misalignment of creator incentives, their enforceability is questionable and can be bypassed through so-called wrapper smart contracts, and the fact that creators benefit from asset volatility (velocity of trading) and speculation rather than fundamental growth and sincere support from their fans. Potential contenders trying to solve these problems are continuous primary offerings and the introduction of a tax system. While continuous primary offering requires the company to continuously produce new content, taxes allow a company to scale revenue based on growth of the economy. There are two tax models currently being explored:

- Harberger tax, under which asset holders value their assets and then pay tax on that value. Unlike real estate taxes where the value of an asset is assessed by a third-party, the Harberger tax base is self-assessed. Under a Harberger tax system, at any point in time, anyone else can buy the asset from the owner at the self-assessed value, forcing a sale. This disincentivizes the owner to undervalue the asset.

- Algorithmic tax, under which the asset value is calculated by advanced machine-learning models based on past trades of assets with similar traits. Tax is paid on the market value of the asset rather than the self-assessed value.

Although there are benefits of the Harberger tax regime, especially the inability of holders to avoid creator payments and optimal value distribution in society, it suffers from considerable drawbacks. The ability of buyers to force a sale questions the existence of actual ownership and breaks the notion of time-compounded return as the early owner does not benefit from future value appreciation, only the creator does. Algorithmic tax calculated based on the market value of the asset is a much better and more fair solution, though due to complexity of building fair and accurate models, it’s too early for production use. DeepNFTValue is a great example of such modelling with future viability.

In either case, we see ways for businesses to monetize assets in open Web 3 creator economies and it is just a matter of time until the optimal solution is found.

RockawayX is positioned to capture value from the metaverse via consumer use cases and infrastructure

At RockawayX, capturing value from the metaverse is in our core investment thesis. As venture investors, we are investing into two key areas:

- Picks and shovels to capture value from the financialization of assets. These would range from straightforward choices of NFT marketplaces, aggregators and valuation platforms to decentralized social networks, product-specific underlying blockchain infrastructure, or gaming middleware.

- Entertainment IP builders that leverage the open economy business model and where creators are empowered to capture the value of their IP. Game creators such as Angry Dynomites Lab or Azra Games that focus on sustainable economics and immersive and collaborative gameplay are great examples of the entertainment IP builders we focus on. Another good example includes interactive digital comic publisher 3 Worlds 3 Moons, where independent creators co-develop the 3 World 3 Moons lore together with the core team. Creators get paid if their stories are read.

It’s time to invest now. The new generation of high performance blockchains, such as Solana, Near, and Ethereum Layer 2s, matured and they are ready to serve the first consumer applications, enabling the growth of the metaverse. Solana can process up to 13,000 transactions per second (TPS), while Near’s theoretical TPS can reach 4,000 to 20,000, and some of Ethereum’s Layer 2’s such as Arbitrum and Optimism currently provide speeds of 2,000-4,000 TPS and are expected to achieve up 40,000 TPS. Layer 1 Ethereum, the original generation blockchain, can process only around 15 TPS. Secondly, a decline in the markets left only committed builders and deeply involved investors remaining in the space, creating downward pressure on company valuations and pushing seed rounds down in value, therefore improving the opportunity for major upside.

Last year, seed rounds with rockstar teams were priced at $30 to $100 million at pre-money valuations (e.g. Star Atlas raising over $10 million, Big Time Studios raising $10.3 million). Today we can close deals with rockstar founders at $8 million to $15 million pre-money. We believe that the combination of headwinds in global financial markets, together with what we think is a temporary decline in interest from the retail and mainstream institutional investor community, will provide an opportunity for investments now to eventually generate 100x returns, just as it was in 2017 with a new wave of layer 1 blockchains, and in 2020 with the rise of decentralized finance.

In the words of Matt Huang, the co-founder of Paradigm:

Authors: Dusan Kovacic (@rampage4551), Tomas Fanta (@tjfanta1)