Summary

- October 2025 was marked by significant macro headwinds and a catastrophic liquidation event in crypto markets. The U.S. Dollar rallied toward 100 as rate cut expectations diminished, pressuring risk assets including crypto and gold. While U.S. equities paradoxically reached new all-time highs, the MSTR mNAV premium reached new lows at ~1.03x

- The defining event occurred on October 10-11 when $19 billion in open interest was erased within 36 hours, liquidating 1.6 million accounts. Triggered by U.S. threats of 100% tariffs on Chinese imports, the crash was amplified by excessive leverage, thin altcoin liquidity, and critical infrastructure failures—particularly Binance's oracle pricing system. Major tokens fell 10-15%, while some altcoins collapsed over 99%. Binance reimbursed users $283 million for collateral mis-pricing that caused erroneous liquidations.

- Despite the turmoil, Solana ETFs attracted steady inflows of $40-70 million daily in their first week, and Solana's blockchain demonstrated technical resilience with low fees and high throughput during the crisis.

- We continue to monitor the MSTR mNAV premium which sits at year to date lows (1.04x) as founder Michael Saylor, apart from the ETFs and copycat DATS, has been the largest and most consistent buyer of BTC over the last several years.

Macro Backdrop

October marked a shift in tone. The U.S. Dollar Index, DXY, rallied to test the 100 level, reversing September’s weakness as the market reduced expectations for further Fed rate cuts after the FOMC meeting at the start of the month.

This stronger USD weighed on risk assets globally, including crypto and gold. Gold initially rallied to $4,380oz on safe-haven flows before retracing as yields stabilized.

The macro narrative of “debasement trade” paused. US Equities, however, continued higher with SPX and NDX making new all-time-highs at the end of October.

Crypto Liquidations on October 10th, and its effects

According to the academic paper “Anatomy of the Oct 10-11, 2025 Crypto Liquidation Cascade”, about $19 billion of open interest was erased within ~36 hours. 1.6 million trader accounts were liquidated and many more will be under water. The crash was very rapid: one article notes that in the first hour of the cascade more than $7 billion of longs were force-closed.

Why did this happen?

- The immediate trigger: a macro shock from a trade-tension announcement (the U.S. threatening 100% tariffs on Chinese imports) which sent risk assets down

- The market was pre-conditioned:

- Very high open interest in derivatives across platforms, meaning a large amount of leveraged exposure.

- Thin liquidity in altcoins and less-traded tokens meant that when things moved, they moved fast.

- The liquidation cascade worked as follows:

- Macro shock triggers price drops

- Margin calls/liquidation events begin

- Sell-pressure adds to price drop

- Lower prices trigger further liquidations (especially in cross-collateral and futures/leveraged positions

- Liquidity fractures (some markets freeze, some tokens mis-price), steep losses

Altcoin impacts

- While the major tokens (Bitcoin, Ethereum) dropped ~10-15% in a short window, many altcoins fared far worse. For example,$ATOM plummeted from $4 to $0.001 (−99.97%) and $SUI from $3.40 to $0.56 (−83.5%”) on Binance.

- That shows how thin-book, less-liquid tokens can have extreme moves when the plumbing breaks.

Binance / Oracle & Collateral Issues

- During the crash, several tokens on Binance such as USDe (Ethena’s stablecoin), BNSOL and wBETH had display issues or de-pegging/mis-pricing.

- Binance’s own post titled “A Deep Dive Into the October 2025 Oracle Failure” discusses a “first-party price oracle” failure, saying:

“On October 10-11, 2025 … this wasn’t a ‘black swan’ event … it was a predictable, systemic failure of a first-party price oracle…” - The oracle failure meant that collateral values and pricing feeds (used for margin/futures collateral, liquidation triggers, etc) were compromised.

- Binance reimbursed users $283 million following the crash, citing that tokens used as collateral had “display glitch” or “de-peg” and structural challenges in collateral management.

- Because traders used these tokens as collateral in futures/margin/loan accounts, mis-pricing triggered automatic liquidations (or margin-calls) even if the token’s real value hadn’t collapsed that quickly.

The chart below shows the drop in open interest:

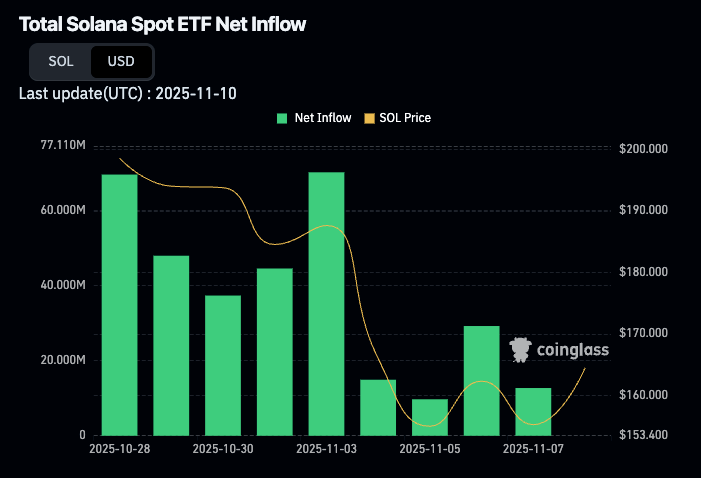

Solana ETF shows inflows despite bearish sentiment

Solana ETFs launched this month and saw steady inflows in the first week, totalling between $40-70M per day collectively. Despite this, SOL has sunk as low as $150 in recent days and ETH inflows are declining rapidly to between $10M-$20M.

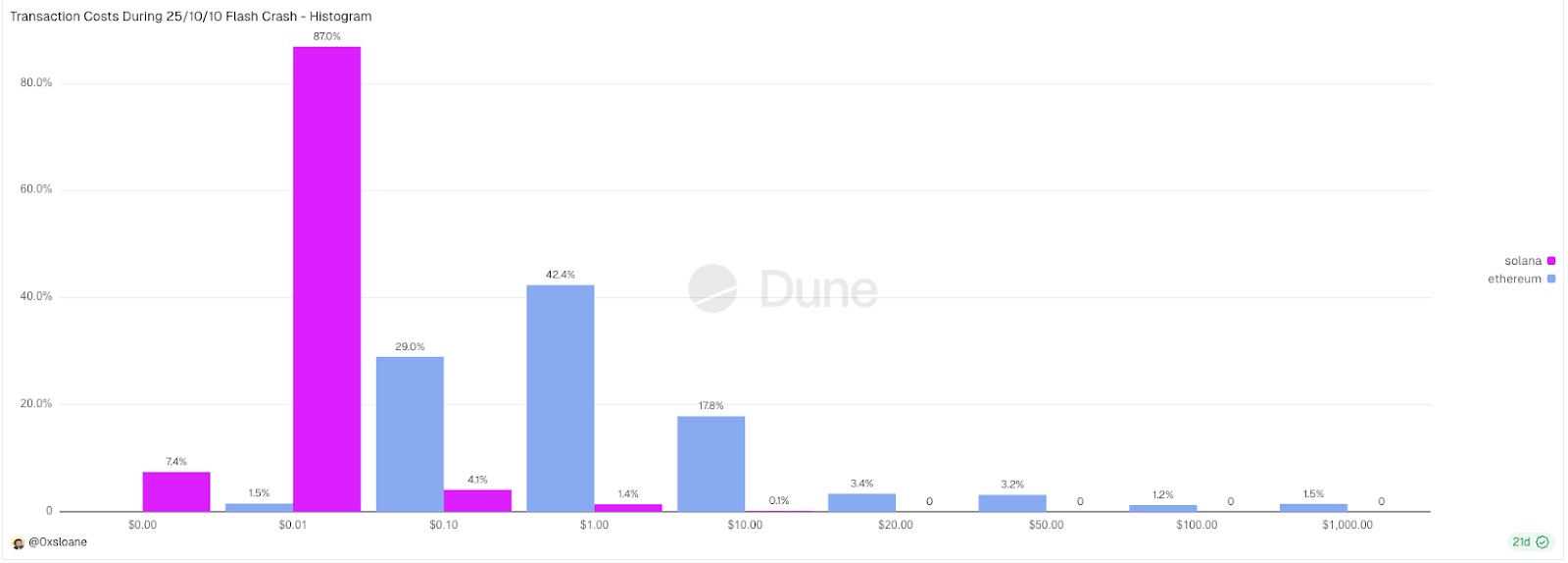

On a positive note, Solana’s technology continued to function during the hour of the flash crash, you’ll see how the distribution of transaction costs compared to Ethereum below:

We can also compare it with other chains, Solana shows the lowest average and median fee whilst maintaining the highest transactions per second:

Conclusion:

The October 2025 liquidation event exposed critical structural vulnerabilities in crypto markets: excessive leverage, fragile infrastructure, and unreliable oracle systems. A routine macro shock escalated into a systemic crisis when Binance's pricing failures triggered cascading liquidations across interconnected margin and collateral systems. The extreme divergence between major tokens (10-15% drops) and illiquid altcoins (near-total losses) revealed persistent liquidity problems in the ecosystem.

However, positive signals emerged. Lending markets, like Kamino Finance, our portfolio company and Solana’s leading DeFi marketplace, and Aave, Ethereum’s dominant lending platform, handled liquidations effectively, and experienced no bad debt. While funding rates in DeFi dried up entirely, they rebounded, and prudent market-neutral investors, like our credit fund, were able to re-enter hedged positions and maintain their exposures.

Solana's technical performance under stress and continued ETF inflows suggest institutional investors are differentiating between market structure failures and blockchain fundamentals. This crisis will likely drive improvements in oracle redundancy, leverage limits, and collateral management; essential steps toward a more resilient crypto infrastructure. Volatility is a fact of this market; but, its maturation depends on preventing technical failures that can amplify market stress into existential crises.

Finally, we view the MSTR mNAV premium as a risk-on / risk off barometer. With mNAV at its lowest point YTD (1.04x) we believe any meaningful bounce in BTC will be preceded with an mNAV expansion.